What happens if a corporation loses money?

A limited liability company (LLC), S corporation, or partnership may also deduct a business loss. If your losses exceed your income from all sources for the year, you have a “net operating loss.” While it’s not pleasant to lose money, a net operating loss can provide crucial tax benefits.

How many years in a row can a business lose money?

In a five-year period, you can claim a business net loss up to two years without any tax problems. If you report operating losses more frequently, the Internal Revenue Service (IRS) might rule your business is only a hobby.

How long can as corporation carry forward losses?

At the federal level, businesses can carry forward their net operating losses indefinitely, but the deductions are limited to 80 percent of taxable income. Prior to the Tax Cuts and Jobs Act (TCJA) of 2017, businesses could carry losses forward for 20 years (without a deductibility limit).

Do you get money back if your business loses money?

Although starting a business can be risky, the tax code provides some protection for business owners who experience financial losses. In general, a business owner whose business loses money can recover some of this loss by using the amount of the loss to create a tax deduction.

Do you get money back if your business takes a loss?

A business loss occurs when your business has more expenses than earnings during an accounting period. The loss means that you spent more than the amount of revenue you made. But, a business loss isn’t all bad—you can use the net operating loss to claim tax refunds for past or future tax years.

What happens if a s Corporation loses 100, 000?

This $100,000 loss–the loss will look like a big deduction on the front of the individual’s tax return–should save anywhere between $10,000 and $50,000 of taxes. One common problem exists, however, with deducting S corporation losses.

What happens to your business if you lose money?

Those losses belong to your corporation. If your losses exceed your income from all sources for the year, you have a “ net operating loss. ” While it’s not pleasant to lose money, a net operating loss can provide crucial tax benefits. It may be used to reduce your tax liability.

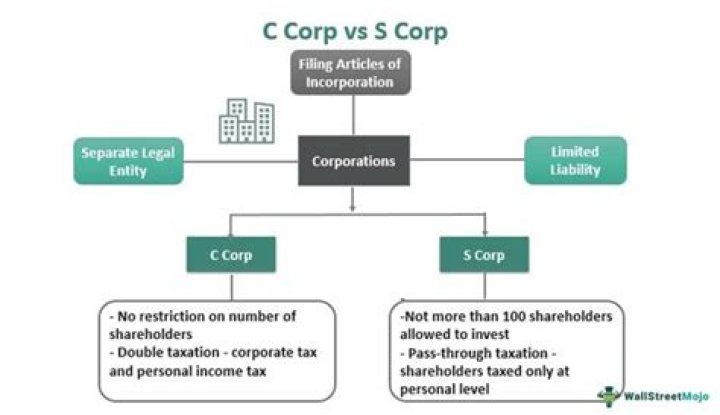

Can a C corporation deduct a business loss?

Yet, if you operate your business through a C corporation, you can’t deduct a business loss on your personal return. Those losses belong to your corporation. If your losses exceed your income from all sources for the year, you have a “ net operating loss.

Is there a limit to how many years a business can lose money?

There’s no limit to how many years your operation can take a loss. Most businesses can’t assume a loss for multiple consecutive years because their money tends to run out. However, if you can comfortably cover your costs and sustain your lifestyle, there’s nothing wrong with maintaining a loss on your business year-over-year.