What happens when an auditor finds a mistake?

Auditors often ignore minor errors and might let you off with a 20 percent penalty, but if they find you guilty of deliberate tax evasion, you might have to pay penalties of up to 75 percent. While auditors are experts at detecting fraud, sometimes an honest mistake can seem like evasion.

What should you do if you think your audit results were incorrect?

Consider outside legal advice to assist in addressing the deficiencies, not in discrediting the audit. Do consider challenging the findings when there are issues that warrant a challenge, not when the parties involved are merely angry at being cited for genuine regulatory findings.

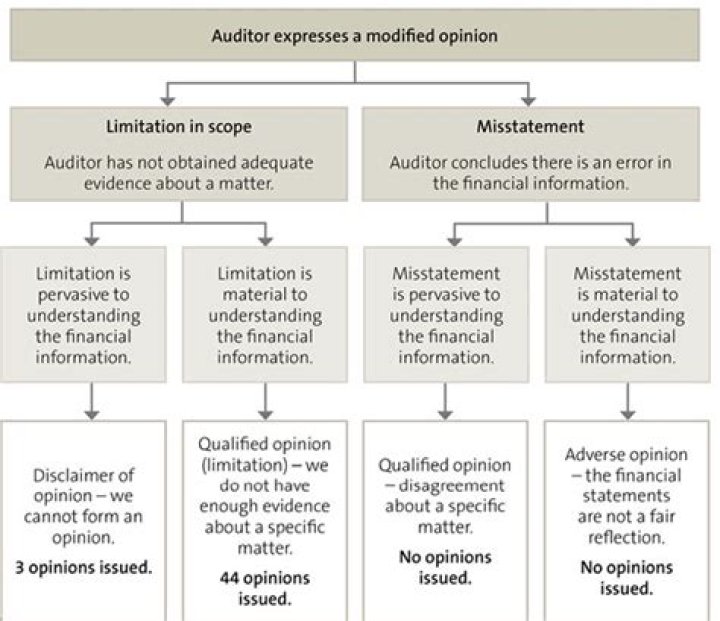

What are auditor’s responsibility for errors and frauds?

The auditor may be held liable for fraud or error. In the audit planning process, the auditor should assess the risk of material misstatement in the financial statements of fraud and error and ask the management of the audited entity for information about any fraud or material error that has been discovered.

Are auditors allowed to make mistakes?

Auditors, alas, are mere humans and subject to mistakes. What happens when mistakes are discovered largely depends on the culture of the individual practice office rather than the norms of the accounting firm.

What happens if get audited?

The IRS will propose taxes and possibly penalties, and you’ll get a “90-day letter” (also known as a statutory notice of deficiency). You’ll have 90 days to file a petition with the U.S. Tax Court. If you still don’t do anything, the IRS will end the audit and start collecting the taxes you owe.

What is mistake in auditing?

When you find misstatements as you perform an audit, you’re responsible for making an assessment. You alone must determine whether the misstatement represents an error or fraud. Errors aren’t deliberate. Fraud takes place when you find evidence of intent to mislead.

What are errors and frauds in auditing?

Errors are innocent or unintentional mistakes while frauds are intentional ones and are preplanned in such a manner that no one can detect them. The most common types of frauds or errors difficult to detect are fraudulent financial reporting, misappropriation of goods, embezzlement of cash and kickbacks.

What are some common mistakes in Audit Reporting?

Receiving feedbacks from clients about reports 4-Pointing Out Problems Only: Another major mistake made in reporting is that audit is built on revealing problems. This situation can be discussed in terms of two main aspects. The first one is about the expectations of management and the positioning of audit function.

How to deal with audit problems-the Auditor?

Educate by stating or restating management’s role in the audit program. Distribute audit reports to management. Have a member of management participate in an audit. Communication is key. We often perceive internal audits or supplier audits as just part of our job, but we need to understand that they play a much larger role.

Why is an accountant called in for a fraud audit?

In a fraud audit, there typically is an allegation of fraud or a fraud has already been discovered; the accountant is called in to gather evidence or to act as an expert witness in connection with legal proceedings relating to the fraud. he or she is not asked to give an opinion on the financial statements as a whole.

When do you need to prepare an audit report?

If the expectation of management from an audit function is simply revealing significant mistakes or an audit report is appreciated only when a fraud is uncovered, this may result in the preparation of audit reports by the auditors from the same perspective, as well.