What impacts FICO score the most?

Top 5 Credit Score Factors

- Payment history. Payment history is the most important ingredient in credit scoring, and even one missed payment can have a negative impact on your score.

- Amounts owed.

- Credit history length.

- Credit mix.

- New credit.

What can be impacted if you have a low FICO score?

Bad Credit Means Trouble Getting a Loan A low score can make it harder to borrow, whether it’s a car loan, mortgage, or credit card account. And if you do qualify, you’ll likely have to pay higher interest rates to make up for your great level of default risk.

How fast can your FICO score go up?

Sure, you’ve made mistakes in your financial past. But, if you pay off debt or fix bad information, the improvements will show up on your credit report within 30 to 45 days, says Andrew Sprauve, a FICO spokesman. Other problems, such as bankruptcy or foreclosure, hurt your score for seven to 10 years.

Why do I have a higher FICO score?

However, if you are using a lot of your available credit, this may indicate that you are overextended—and banks can interpret this to mean that you are at a higher risk of defaulting. In general, a longer credit history will increase your FICO Scores.

How does credit mix affect your FICO score?

Your credit mix accounts for about 10% of your FICO credit score. Credit mix means having different types of credit accounts, such as credit cards, a car loan, and a mortgage, and this plays a small role in determining your FICO Scores.

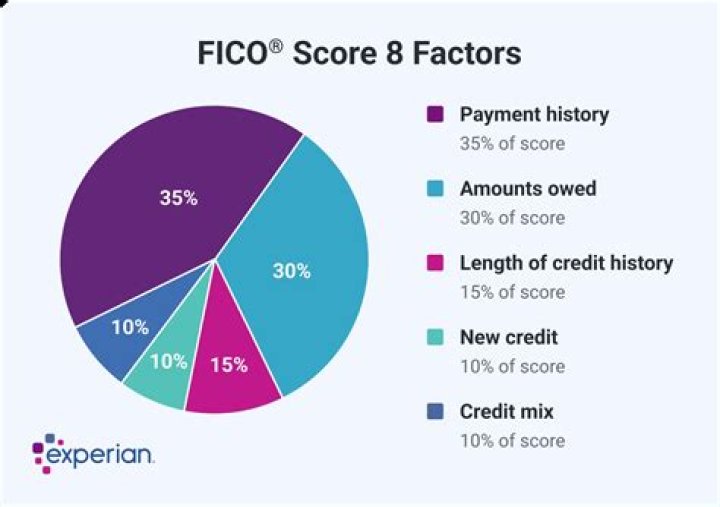

What makes up 35% of my FICO score?

This data is grouped into five categories: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%) and credit mix (10%).

How are FICO scores based on credit history?

This data is grouped into five categories: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%) and credit mix (10%). The percentages in the chart reflect how important each of the categories is in determining how your FICO Scores are calculated.