What is a 1065 partnership?

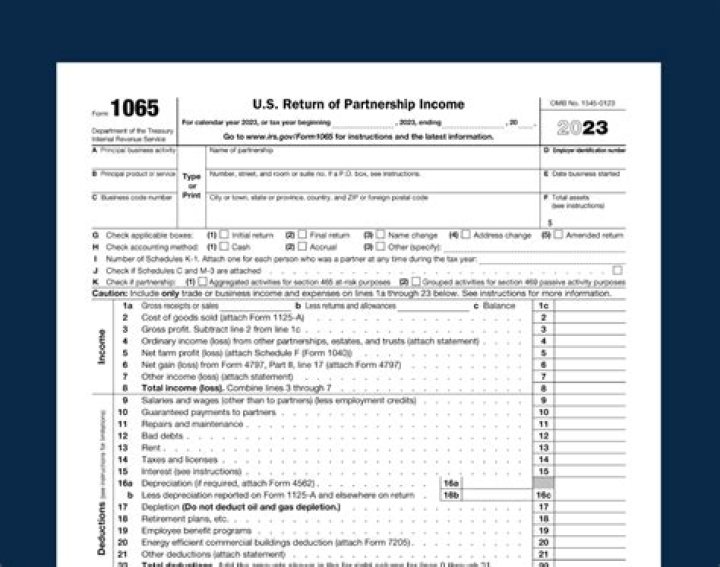

IRS Form 1065 is used to declare profits, losses, deductions, and credits of a business partnership for tax filing purposes. This form is filed by LLCs, foreign partnerships with income in the U.S., and nonprofit religious organizations. Partnerships must also submit a completed Schedule K-1.

Do partners in a partnership pay income tax?

A partnership must file an annual information return to report the income, deductions, gains, losses, etc., from its operations, but it does not pay income tax. Instead, it “passes through” profits or losses to its partners. For deadlines, see About Form 1065, U.S. Return of Partnership Income.

Is a 1065 a general partnership?

All business partnerships must file Form 1065. A partnership agreement could define your entity as a general partnership, limited partnership, limited liability partnership, LLC, etc. It’s important to note that all partnerships act as “pass-through” entities.

When to file Form 1065 for a partnership termination?

If a partnership terminates before the end of what would otherwise be its tax year, IRS Form 1065 must be filed for the short period. There are two types of tax terminations of partnerships: real and technical.

Who is the designated tax matters partner in a partnership?

Under the old rules, a partnership, subject to the rules for consolidated audit proceedings in sections 6221 through 6234, would designate a partner as the Tax Matters Partner for the tax year for which the return is filed. The designated tax matter partner was required to be a general partner, and in most cases, also must be a U.S. citizen.

Do you have to file Form 8865 for domestic partnership?

Domestic partnerships that transfer property to foreign partnerships need only file one Form 8865 for the entire partnership; each domestic partner does not need to file a separate Form 8865. Persons who qualify as filers under both Category 3 and 4 need only file under Category 3.

When to use Form 1065 or form 8865?

Filing of Form 1065 by the foreign partnership allows Category 1 and 2 filers to use the schedules from the Form 1065 filing in place of the equivalent schedules required under Form 8865. Establishing foreign partnerships in a legal and efficient way is not as complicated as it may seem.