What is a change in accounting principle and how is it reported?

A change in accounting principle is defined as: “A change from one generally accepted accounting principle to another generally accepted accounting principle when (a) there are two or more generally accepted accounting principles that apply; or (b) the accounting principle formerly used is no longer generally accepted.

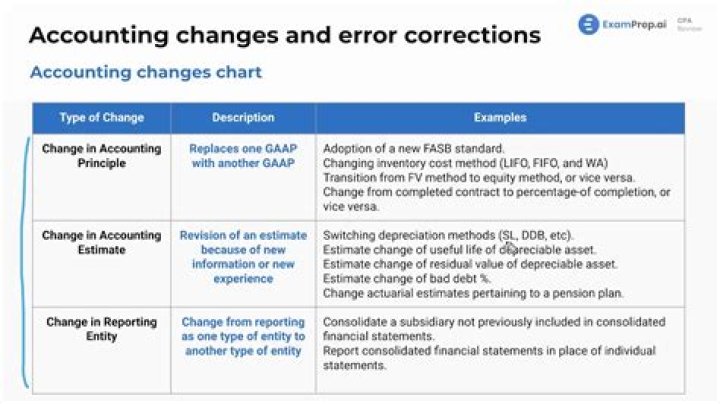

Is a change in reporting entity a change in accounting principle?

Accounting changes and error correction refers to the guidance on reflecting accounting changes and errors in financial statements. Accounting changes are classified as a change in accounting principle, a change in accounting estimate, and a change in reporting entity.

How is change in reporting entity reported?

Change in reporting entity. Accounting changes that result in financial statements of a different reporting entity are reported retrospectively by restating all prior periods.

How should the effect of a change in accounting estimates be accounted for?

Changes in estimates continue to be accounted for prospectively. CPAs should account for them in (a) the period of change if the change affects only that period or (b) the period of change and future periods if the change affects both. Prior periods are not restated and pro forma amounts are not reported.

What is considered a change in accounting principle?

A change in accounting principle is the term used when a business selects between different generally accepted accounting principles or changes the method with which a principle is applied. Accounting principles impact the methods used, whereas an estimate refers to a specific recalculation.

Which of the following is a change in accounting principle?

An example of a change in accounting estimate that is effected by a change in accounting principle is a change in: depreciation methods. Which of the following is a change in accounting estimate? Change in actuarial calculations pertaining to pension plan.

Which of the following is considered a change in reporting entity?

Which of the following constitutes a change in reporting entity? A change in reporting entity occurs when one company acquires another.

What do you need to know about change in accounting principle?

In the period in which a company makes a change in accounting principle, it must disclose on the financial statements the nature of the change, its justification, and its effect on net income. Also, the company must show on the income statement for the year of the change and the cumulative effect of the change on prior years’ income (net of tax).

Can a company retrospectively apply a change in accounting principle?

Under Statement no. 154, companies must retrospectively apply all voluntary changes in accounting principle to previous-period financial statements unless doing so is impracticable or FASB mandates another approach.

What happens after a change in accounting policy?

After the change, it looks like the financial statement has been prepared base on the new policy since the beginning. All adjustment impact to income statement since the beginning will be adjusted to the retained earnings. There will an adjustment in the beginning balance of retained earnings in the comparative statement of change in equity.

When to restate financial statements due to change in principle?

Statement no.154 requires that prior financial statements issued for comparative purposes be restated for the direct effects of the change in principle. If ABC reissues its 20X5 statements for comparative purposes with 20X6, it must restate the 20X5 income statement to what it would have been had the company used FIFO.