What is a loss run in insurance?

An insurance loss run is a document that records the history of claims made against a business insurance policy, much akin to an incident report. The report is a document you can provide to prospective insurers when shopping for new business insurance coverage.

Do insurance companies have to provide loss runs?

In most states a company is legally required to provide your loss runs within ten business days. In some cases, you will be asked to provide loss-run reports every year, even if your policy is insured with the same company.

What does currently valued loss runs mean?

Many state regulations dictate that a carrier must fulfill a loss run report request within ten days. So, you won’t usually be waiting for ages to receive this information. What’s more; is that a loss run report must be currently valued, which means the information was generated within the past 30 days.

How long does an insurance company have to provide loss runs?

However, since each state regulates the insurance industry operating within its borders, there are state laws requiring companies to provide loss run reports within specified timeframes, often just 10 days.

How are loss runs calculated?

It is calculated by assessing the likely medical, indemnity and other expenses of each injury or occupational disease. Insurance carriers try to calculate the expected costs of a claim as accurately as possible. However, the reserve amount could potentially be higher or lower than what ultimately gets paid out.

Why do insurance companies need loss runs?

Insurance loss runs refer to your business insurance claims history. Much like credit scores allow banks to determine whether you’re a good candidate for a bank loan or credit card, loss runs allow insurers to assess how risky your business will be to insure.

What is the average validity of a loss Runs report?

Typically, an insurance company will ask for the loss run report that includes up to 5 years of history or for how long coverage was provided.

What is a business loss run?

Loss Run reports provide a summary of a small business’ insurance claims history, including the types of claims filed in the past, the frequency of past claims filed and the related costs. This data is used by insurers to help figure out how risky a business is to insure.

How do you find a loss run?

How can I get a loss run report? Just contact your account manager, agency, or insurer and tell them you need a loss run report. Specify how many years of claims history you need and your deadline for receiving the information.

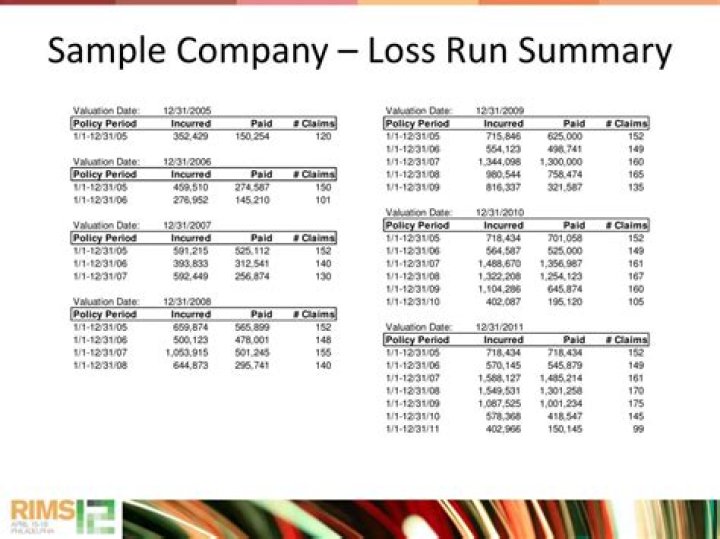

What is a loss run summary?

Loss Run reports provide a summary of a small business’ insurance claims history, including the types of claims filed in the past, the frequency of past claims filed and the related costs. This data is used by insurers to help figure out how risky a business is to insure. The higher the risk, the higher the premium.

How does a professional liability insurance policy work?

Typical professional liability policies will indemnify the insured against loss arising from any claim or claims made during the policy period by reason of any covered error, omission or negligent act committed in the conduct of the insured’s professional business during the policy period.

What is the purpose of a loss run report?

A loss run is a report generated by your insurance company showing the claim activity on each of your insurance policies. The loss run serves a number of purposes, including the following: Informational: Gives you a detailed account of the claims activity on your policy during a given policy term or terms.

How long does insurance company have to give loss run report?

Which is the best type of professional liability insurance?

Indemnity insurance is an agreement wherein one party guarantees compensation for losses or damages incurred by another. Errors and omissions insurance is a type of professional liability insurance that protects against claims of inadequate work or negligent actions.