What is a post adjustment trial balance?

An adjusted trial balance is prepared after adjusting entries are made and posted to the ledger. This is the second trial balance prepared in the accounting cycle. Its purpose is to test the equality between debits and credits after adjusting entries are made, i.e., after account balances have been updated.

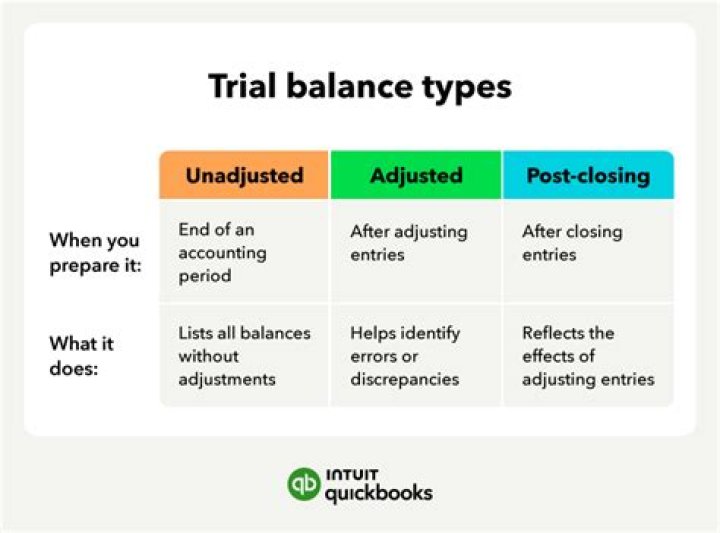

What is adjusted and unadjusted trial balance?

Meaning. Unadjusted trial balance is the first list of ledger account balances, compiled without making any period end adjustments. Adjusted trial balance is the trial balance compiled after considering adjustment entries at the close of the accounting period.

How are entries added to an adjusted trial balance?

In this adjustment, entries are directly added to the unadjusted trial balance to convert it to an adjusted trial balance. The main purpose of adjusted trial balance is a document that shows the total amount of debt against the total amount of credit. This is not considered as a financial statement, because it is only used as an internal document.

When do you need to treat adjustment entries twice?

In a case when he makes the adjustment entries after preparation of trial balance, he needs to treat each of the adjustment twice while preparing trading and profit and loss account and balance sheet. In case adjustment entries made before preparation of trial balance, such adjustment appears in the trial balance.

How to prepare your adjusting entries step by step?

How to prepare your adjusting entries. 1 Step 1: Recording accrued revenue. Any time that you perform a service and have not been able to invoice your customer, you will need to record the 2 Step 2: Recording accrued expenses. 3 Step 3: Recording deferred revenue. 4 Step 4: Recording prepaid expenses. 5 Step 5: Recording depreciation expenses.

When do journal entries need to be adjusted?

What are Adjusting Entries? Adjusting entries are journal entries that are made in the accounting journals at the end of an accounting period after the preparation of the trial balance.