What is a specific audit?

A special audit is a tightly-defined audit that only looks at a specific area of an organization’s activities. This type of audit may be initiated by a government agency, but could be authorized by any entity, or even internally.

When books are required to be audited?

Where the income is more than Rs 1,20,000 or total sales, turnover or gross receipts are more than 10,00,000 in all preceding 3 years, such profession or businesses must maintain books of accounts and other documents which may enable the Assessing Officer to calculate their taxable income as per the Income Tax Act.

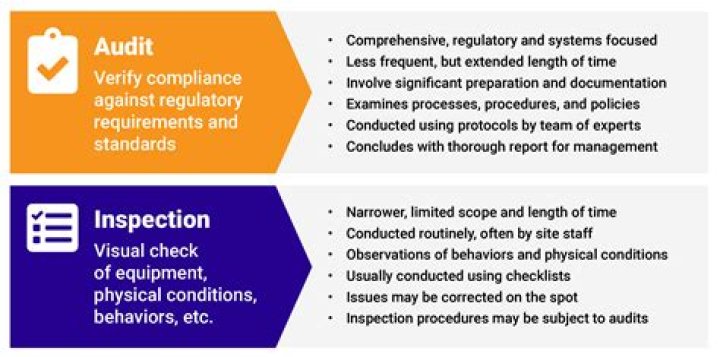

What are the objects of audit?

The objective of an audit is to express an opinion on financial statements. The auditor has to verify the financial statements and books of accounts to certify the truth and fairness of the financial position and operating results of the business.

Who needs to audit?

As per section 44AB, following persons are compulsorily required to get their accounts audited : A person carrying on business, if his total sales, turnover or gross receipts (as the case may be) in business for the year exceed or exceeds Rs. 1 crore.

Who can audit books?

The Income Tax laws make it a point for the taxpayers in high-income businesses or professions to maintain their books of their accounts as per Section 44AA and the books should be further audited by a Chartered Accountant as per section 44AB.

Why do I need to audit my books of accounts?

The Income Tax laws make it a point for the taxpayers in high-income businesses or professions to maintain their books of their accounts as per Section 44AA and the books should be further audited by a Chartered Accountant as per section 44AB. The audit report is prepared as a proof of the audit which ensures that all the accounts are verified.

What should be included in the audit evidence?

The audit evidence generated by the planned audit procedures should be sufficient and appropriate to support and corroborate, or to contradict, the management’s assertions in respect of specific classes of transactions, account balances or disclosures in the financial statements.

What do you need to know about an audit?

Learn everything you need to know about the financial investigations into your business. We’ll teach you about the 3 types of audits there are, how to properly prepare for an audit, how they can affect your business, how to find the right auditor, and more. What is an internal audit?

Who is the author of the book audit?

This book is authored by Maire Loughran; the first edition was Originally written in 2010 and published by John Wiley & Sons. This book succeeded in presenting audit in the simplest picture for someone who aspires to learn what auditing is all about.