What is a spot rate finance?

What Is the Spot Rate? The spot rate is the price quoted for immediate settlement on an interest rate, commodity, a security, or a currency. The spot rate, also referred to as the “spot price,” is the current market value of an asset available for immediate delivery at the moment of the quote.

What is the one year forward rate for a 1 year period?

The one year forward rate represents the one-year interest rate one year from now. You would solve the formula (1.04)^2=(1.02)(1+F). F is 6.03%.

What is short rate and spot rate?

Spot versus Short Rates Spot rate: Short rate: • Refers to the interest rate that prevails over a specific time period.

What is the 1 year spot rate?

Spot Interest Rate vs Yield to Maturity The spot interest rates for 1, 2 and 3 years are 1.50%, 1.75% and 1.95%.

How do you calculate spot rate?

The spot rate is calculated by finding the discount rate that makes the present value (PV) of a zero-coupon bond equal to its price. These are based on future interest rate assumptions. So, spot rates can use different interest rates for different years until maturity.

How do you calculate forward rates?

To calculate the forward rate, multiply the spot rate by the ratio of interest rates and adjust for the time until expiration. So, the forward rate is equal to the spot rate x (1 + domestic interest rate) / (1 + foreign interest rate).

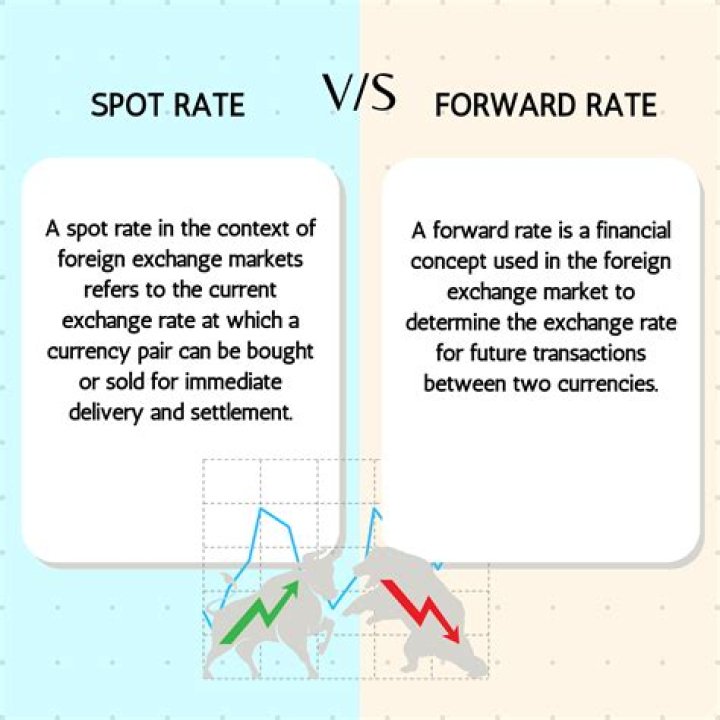

What is the difference between spot rate and forward rate?

In commodities markets, the spot rate is the price for a product that will be traded immediately, or “on the spot.” A forward rate is a contracted price for a transaction that will be completed at an agreed upon date in the future.

What is the difference between forward rate and short rate?

Note the crucial distinction between a short rate and forward rate: the short rate refers to a rate that is set either today (in the case of r1) or in the future (in the case of all other short rates); the forward rate always refers to a rate that is set today, even though the time period of the loan may be some time …

What is the current spot rate for 1 year?

Suppose the current forward curve for 1-year rates is 0y1y=2%, 1y1y=3%, and 2y1y=3.75%. The 2-year and 3-year implied spot rates are, respectively: The correct answer is A. The 2-year and 3-year implied spot rates are 2.5%, and 2.91% respectively.

What are the 2 year and 3 year interest rates?

The correct answer is A. The 2-year and 3-year implied spot rates are 2.5%, and 2.91% respectively. Define forward rates and calculate spot rates from forward rates, forward rates from spot rates, and the price of a bond using forward rates

What’s the difference between 2 year and 3 year bond?

The correct answer is A. The 2-year and 3-year implied spot rates are 2.5%, and 2.91% respectively. Define forward rates and calculate spot rates from forward rates, forward rates from spot rates, and the price of a bond using forward rates.

How to calculate the one year forward rate?

The spot rate for two years, S 1 = 7.5% The spot rate for one year, S 2 = 6.5% No. years for 2 nd bonds, n 1 = 2 years No. years for 1 st bonds, n 2 = 1 year As per the above-given data, we will calculate a one-year rate from now of company POR ltd. Therefore, the calculation of the one-year forward rate one year from now will be,