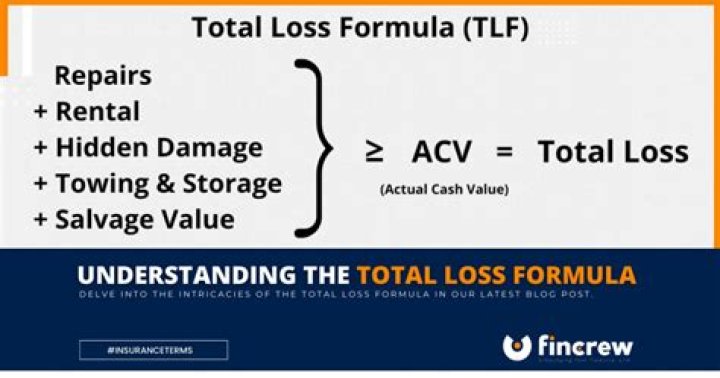

What is a total loss formula?

The total loss formula (TLF) is the second method for determining when a car is a total loss. It equals the fair market value of a vehicle minus its salvage value. If the cost of repairs exceeds the TLF outcome, the insurance company can declare it a total loss.

Can I sue my insurance company for total loss?

You can always sue the insurance company. However insurance company is only liable for the vehicles value if it is a total loss which it appears in this case. They are not required to buy you new car. However what a similar car costs is proof of value.

Is it worth keeping a totaled car?

Safety should be your primary concern when keeping a totaled car. If damage to the totaled vehicle is mostly cosmetic, you may be able to put it back into service for a modest cost. However, if fixing the car means reaching deep into your pockets, you may be better off letting it go.

Can you keep your car if it’s a total loss?

A car is considered a total loss, or “totaled,” if the cost of repairing it after an accident is more than the value of the vehicle. You can choose to keep a total loss vehicle instead if you want to repair it or salvage its parts on your own.

Is frame damage a total loss?

The determination that an automobile has endured frame damage is an unpleasant surprise to say the least. If this determination is made by your insurance company or automotive technician, you might assume your vehicle is totaled. However, frame damage does not guarantee the vehicle is considered a total loss.

Can you buy back a totaled vehicle?

Many insurers will allow you to “buy back” a vehicle they have totaled out if you wish to repair it and make it roadworthy again. If you wish to buy back a car from an insurance company that deemed your vehicle a total loss you should discuss the value of the car and the cost to buy it back.

How to claim losses from a small business on taxes?

Business Losses. How you claim a business loss depends on the business form. Sole proprietors calculate business profits and losses on Schedule C of Form 1040. If business expenses exceed revenues, the owner has a net operating loss that offsets other sources of income on the 1040.

Can a C corporation claim a business loss?

These “rules” limit how much you can claim from a business loss based on your amount at risk in the business. These rules apply to S corporation shareholders, partners, and some C corporation owners. Specific types of businesses are also subject to these rules.

Can a bank participate in a total loss claim?

Whether the bank or loan company has any rights to participate in your total loss claim. This usually only occurs when you are making the claim against your insurance company. If you are making a claim against the other driver’s insurance company, they can issue payment to a registered owner (you?) of your car.

Can a sole proprietor claim a net operating loss?

If your small business had a net operating loss, you can claim the loss on your individual tax return. How you claim a business loss depends on the business form. Sole proprietors calculate business profits and losses on Schedule C of Form 1040.