What is accounting cycle and explain its steps?

The accounting cycle is the process of accepting, recording, sorting, and crediting payments made and received within a business during a particular accounting period. Once all the business accounts have been balanced, they are closed out for that period and new ones created for the next accounting period.

What is the best job in accounting?

Top accounting jobs

- Accounting clerk. National average salary: $16.09 per hour.

- Bookkeeper. National average salary: $17.37 per hour.

- Credit analyst. National average salary: $57,373 per year.

- Compliance officer. National average salary: $62,771 per year.

- Auditor.

- Personal finance advisor.

- Budget analyst.

- Financial analyst.

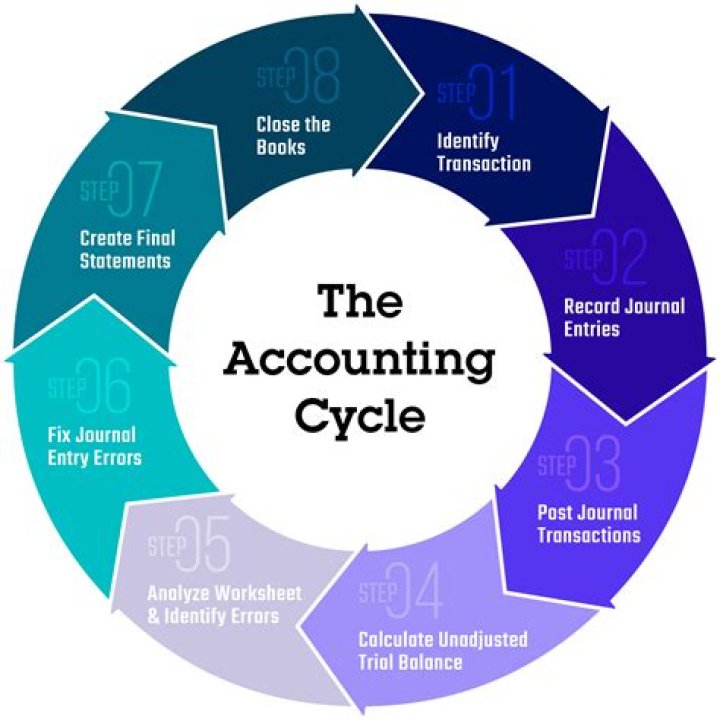

What are the 9 steps of accounting cycle?

9 Steps of the Accounting Cycle

- Collection of data and analysis of transactions.

- Journalizing.

- Recording the journals into the ledger accounts.

- Creating an unadjusted trial balance.

- Performing adjusting entries.

- Creating adjusted trial balance.

- Creating financial statements from the trial balance.

- Closing the books.

How many steps are there in the accounting cycle?

These processes are rotated continuously in every accounting period. So, it is said that the accounting cycle is the continuous process of recording and processing of all transactions of an organization. Ten (10) steps of the accounting cycle are as follows:

How are transactions recorded in the accounting cycle?

To simplify the recording process, special journals are often used for transactions that recur frequently such as sales, purchases, cash receipts, and cash disbursements. A general journal is used to record those that cannot be entered in the special books. Transactions are recorded in chronological order and as they occur.

Which is not accounted for in the accounting cycle?

For example, a personal loan made by the owner that does not have anything to do with the business entity is not accounted for. The transactions identified are then analyzed to determine the accounts affected and the amounts to be recorded. The first step includes the preparation of business documents, or source documents.

Which is the second stage of the accounting cycle?

The second stage in the accounting cycle is posting entries from journal to the ledger account. Ledger is the principal book of accounting system. Whereas, journal is the original book of entry. General Ledger consists of numerous accounts in which transactions pertaining to these accounts are recorded.