What is adjusting entries and its types?

Adjusting entries update previously recorded journal entries to match expenses and revenues with the accounting period that they occur. These entries are only made when using the accrual basis of accounting. There are three main types of adjusting entries: accruals, deferrals, and non-cash expenses.

What are adjusting entries Why are adjusting entries necessary?

Adjusting entries are necessary to update all account balances before financial statements can be prepared. These adjustments are not the result of physical events or transactions but are rather caused by the passage of time or small changes in account balances.

What are the different types of adjusting entries?

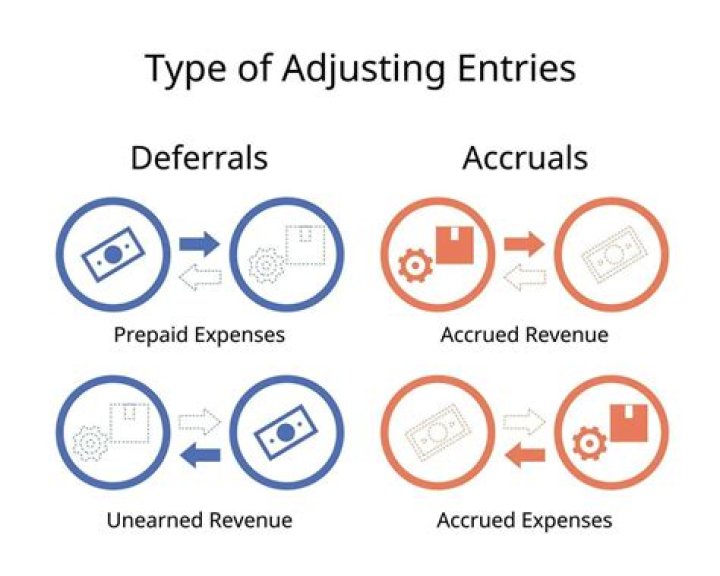

The following entries are the most common types of adjusting entries recorded in books of accounts.

What are the different types of journal entries?

Adjusting Entries: Definition, Types and Examples 1 Definition of Adjusting Entries. Adjusting entries refers to a set of journal entries recorded at the end of the accounting period to have an updated and accurate balances of all 2 Importance of Adjusting Entries. 3 Types of Adjusting Entries. 4 Examples of Adjusting Entries. …

When is an entry in a journal an adjusting entry?

Adjusting entries affect one real account and at least one nominal account. We should note that not all entries, recorded by the business at the end of an accounting year, are adjusting journal entries. For instance, an entry for a purchase or a sale made on the last day of the fiscal period is not an adjusting entry.

When do you adjust entries in an accounting cycle?

Adjusting entries. Posted in: Accounting cycle (explanations) Adjusting entries (also known as end of period adjustments) are journal entries that are made at the end of an accounting period to adjust the accounts to accurately reflect the revenue and expenses of the current period.