What is allowance for doubtful receivables?

An allowance for doubtful accounts is a contra account that nets against the total receivables presented on the balance sheet to reflect only the amounts expected to be paid. The allowance for doubtful accounts estimates the percentage of accounts receivable that are expected to be uncollectible.

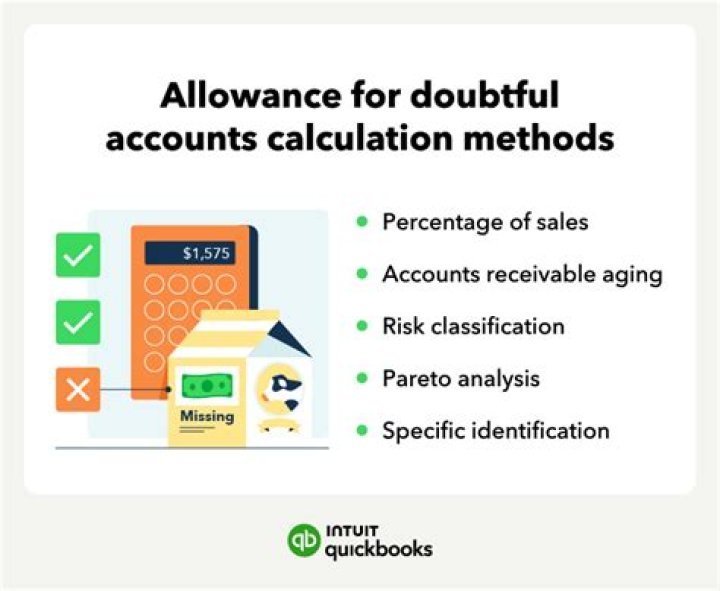

How do you calculate allowance for doubtful accounts?

Another method for estimating the allowance for doubtful accounts is to group all of the company’s outstanding accounts receivable by the age of the debt and then apply different percentages to each group. The total would reflect the predicted unpaid amount.

Where does allowance for doubtful debts go in the balance sheet?

Doubtful accounts are an asset. The amount is reflected on a company’s balance sheet as “Allowance For Doubtful Accounts”, in the assets section, directly below the “Accounts Receivable” line item.

What increases allowance for doubtful accounts?

Allowance for doubtful accounts journal entry To predict your company’s bad debts, create an allowance for doubtful accounts entry. To do this, increase your bad debts expense by debiting your Bad Debts Expense account. Then, decrease your ADA account by crediting your Allowance for Doubtful Accounts account.

How do you reduce allowance for doubtful accounts?

Allowance for Doubtful Debts Adjustment When you receive money you wrote off as uncollectable, you must reverse the write-off entry and record the payment. Reverse the write-off entry by increasing the accounts receivable account with a debit and decreasing the allowances for doubtful accounts account with a credit.

How many types of allowances are there in salary?

In terms of taxability there are three types of allowances; Taxable Allowance, it is the Allowance which is fully taxable. Partially Taxable Allowance is the Allowance in which some part is exempt, and some part is taxable. Non-Taxable Allowance, is the Allowance which is fully exempt from tax.