What is an example of an accrued revenue?

The most common example of accrued revenue is the interest income (earned on investments but not yet received) and accounts receivables (the amount due to a business for unpaid goods or services.)

What are three examples of accrued revenue?

The two most common forms of accrued revenues are interest revenue and accounts receivable. Interest revenue is income that’s earned from investments made. Accounts receivable is money owed to a company for goods or services that have not been paid for yet.

What is the entry for accrued income?

The Journal entry to record accrued incomes is: Amount (Cr.) Dr. The Accrued Income A/c appears on the assets side of the Balance Sheet. While preparing the Trading and Profit and Loss A/c we need to add the amount of accrued income to that particular income.

Is cash accrued revenue?

Accrued revenue refers to a company’s revenue that has been earned through a sale that has already occurred, but the cash has not yet been received from the paying customer.

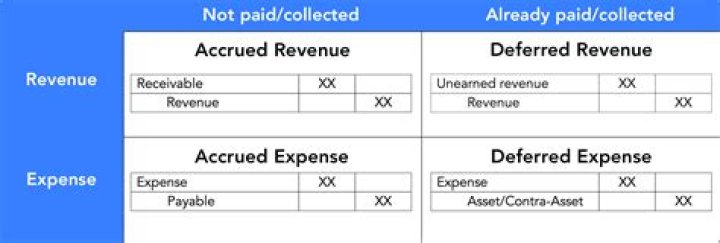

What is the difference between accrued revenue and unearned revenue?

While accrued revenue is capital not earned on services already provided, unearned revenue is capital already earned on services not yet provided.

When do you accrue revenue for a company?

Companies can accrue revenues as future sales transactions are completed over time. Under the expense recognition principles of accrual accounting, expenses are recorded in the period by which they were incurred and not paid.

Where does a bill payable go in accounting?

Recording a Bill Payable. Under the accrual method of accounting or bookkeeping, a bill payable or unpaid vendor invoice is recorded in Accounts Payable with a credit entry.

Do you have to pay cash for expense accrual?

Thus, expense accruals don’t require corporations make cash payments to pay for an expense on the time of a transaction. Without accruing bills, corporations mismatch bills with revenues, overstating revenues in some periods and understating revenues in different durations.

When is Commission payout recorded in accrual accounting?

Let’s assume the clerk is entitled to collect a 10% commission on the sale, which the customer ultimately pays for in April. According to accrual accounting rules, the boutique must record the $2,000 outgoing commission payout to the clerk, in its February’s expense reports, even though the clerk won’t pocket the money until two months later.