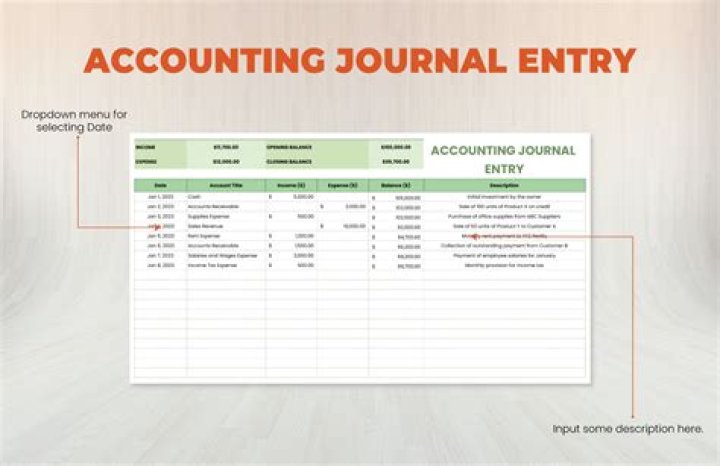

What is bookkeeping and journal entries?

Bookkeeping journals are where a business records its daily financial transactions in date order showing which accounts to debit or credit with journal entries. Books of original entry – these are the first place the transactions are recorded using the information taken from accounting source documents.

What is general journal in bookkeeping?

Simply defined, the general journal refers to a book of original entries, in which accountants and bookkeepers record raw business transactions, in order according to the date events occur.

What are bookkeeping journals and entries in business?

Bookkeeping journals are where a business records its daily financial transactions in date order showing which accounts to debit or credit with journal entries. This is much like personal journals in which people record the events that happen in their life in date order. Day books – these books are used on a daily basis

Is the general journal a double entry book?

The general journal is a book of prime entry and the entries in the journal are not part of the double entry posting. Typically, the general journal entries record transactions such as the following:

What do you need to know about journal entries?

Journal entries are the very first step in the accounting cycle. The main thing you need to know about journal entries in accounting is that they all follow the double-accounting method. What this means is that for every recorded transaction, two accounts are affected – and as a result, there is always a debit entry and a credit entry.

What is the purpose of an accounting journal?

They are chronological accounting records, each one composed of a debit and a credit. What is the Purpose of Journal Entries? The purpose of journal entries is to keep a day-to-day, chronological record of a business and its transactions. What Do Journals Look Like? If you’re not yet familiar with journal entries, don’t worry!