What is break-even analysis used for?

Put simply, break-even analysis helps you to determine at what point your business – or a new product or service – will become profitable, while it’s also used by investors to determine the point at which they’ll recoup their investment and start making money.

How do you think you would use break-even analysis?

A break-even analysis is a useful tool for determining at what point your company, or a new product or service, will be profitable. Put another way, it’s a financial calculation used to determine the number of products or services you need to sell to at least cover your production costs.

What is an example of breakeven?

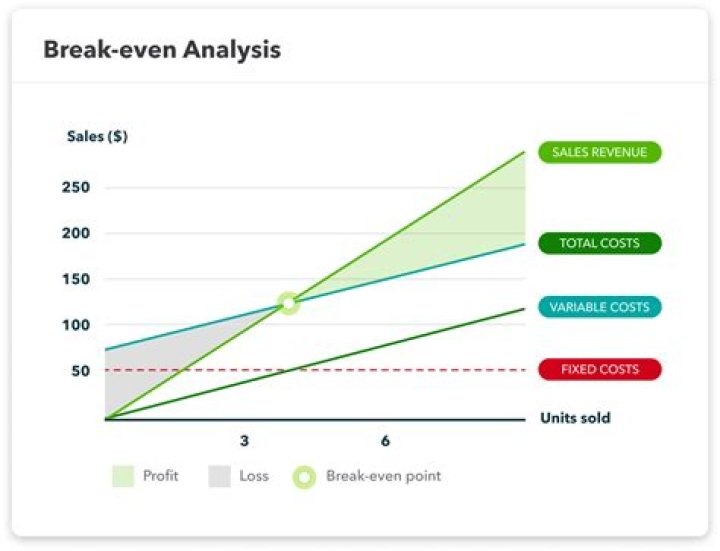

For example, selling 10,000 units would generate 10,000 x $12 = $120,000 in revenue. If the company sells 10,000 units, the company would incur 10,000 x $2 = $20,000 in variable costs and $100,000 in fixed costs for total costs of $120,000. The break even point is at 10,000 units.

When to use breakeven analysis in business planning?

A breakeven analysis determines the sales volume your business needs to start making a profit, based on your fixed costs, variable costs, and selling price. It often is used in conjunction with a sales forecast when developing a pricing strategy, either as part of a marketing plan or a business plan .

What do you need to know about break even?

Break-even analysis uses a calculation called the break even point (BEP) which provides a dynamic overview of the relationships among revenues, costs, and profits. More specifically, it looks at a company’s fixed costs in relation to profits that are earned from each unit sold. Typical variable and fixed costs differ widely among industries.

Which is the formula for break even analysis?

Formula for Break Even Analysis The formula for break even analysis is as follows: Break even quantity = Fixed costs / (Sales price per unit – Variable cost per unit)

How to calculate break even point from costs and revenues?

How to Calculate Break-Even Point Volume From Costs and Revenues in 5 Steps. Break-even analysis finds break-even volume by analyzing relationships for fixed and variable costs on the one hand, and business volume, pricing, and net cash flow on the other.