What is considered like-kind in a 1031 exchange?

Like-kind properties are real estate assets of a similar nature that can be exchanged without incurring any tax liability under Section 1031 of the Internal Tax Code. Primary residences do not qualify for a 1031 exchange. Properties must be held in the United States in order to qualify as like-kind.

What type of property qualifies for Section 1031 exchange?

Under the Tax Cuts and Jobs Act, Section 1031 now applies only to exchanges of real property and not to exchanges of personal or intangible property. An exchange of real property held primarily for sale still does not qualify as a like-kind exchange.

What qualifies as a 1031 property?

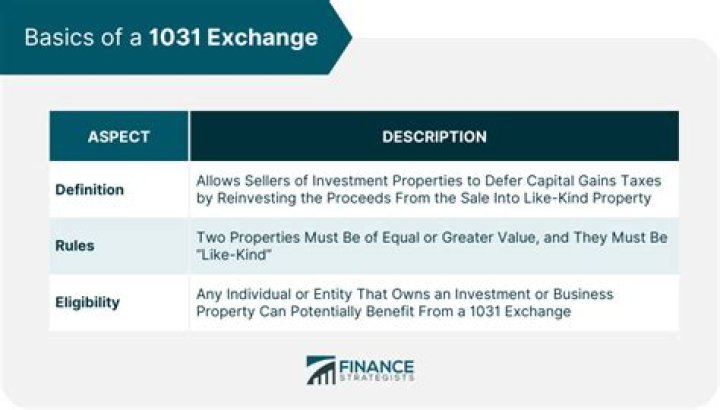

The main requirements for a 1031 exchange are: (1) must purchase another “like-kind” investment property; (2) replacement property must be of equal or greater value; (3) must invest all of the proceeds from the sale (cannot receive any “boot”); (4) must be the same title holder and taxpayer; (5) must identify new …

How much time do you have to complete a 1031 exchange?

To receive the full benefit of a 1031 exchange, your replacement property should be of equal or greater value. You must identify a replacement property for the assets sold within 45 days and then conclude the exchange within 180 days. There are three rules that can be applied to define identification.

IRC Section 1031 does not limit “like-kind” property to certain types of real estate. Any real property held for productive use in a trade or business or for investment can be considered “like-kind” property. The term refers to the nature or character of the property, rather than its grade or quality.

What is like kind exchange in IRC Section 1031?

IRC Section 1031 Like-Kind Exchange Under Section 1031 of the Internal Revenue Code (IRC), owners of business or investment properties, through the use of a Qualified Intermediary, can sell one property and purchase a similar or “like-kind” property while deferring capital gains.

What do you need to know about the 1031 exchange?

Key Takeaways. A 1031 exchange is a swap of properties that are held for business or investment purposes. The properties being exchanged must be considered like-kind in the eyes of the IRS for capital gains taxes to be deferred. If used correctly, there is no limit on how many times or how frequently you can do 1031 exchanges.

What does section 1031 of the Internal Revenue Code mean?

Under Section 1031 of the Internal Revenue Code (IRC), owners of business or investment properties, through the use of a Qualified Intermediary, can sell one property and purchase a similar or “like-kind” property while deferring capital gains.

Can a 1031 exchange apply to a former primary residence?

The 1031 provision is for investment and business property, although the rules can apply to a former primary residence under certain conditions.