What is equal to fixed cost at break-even point?

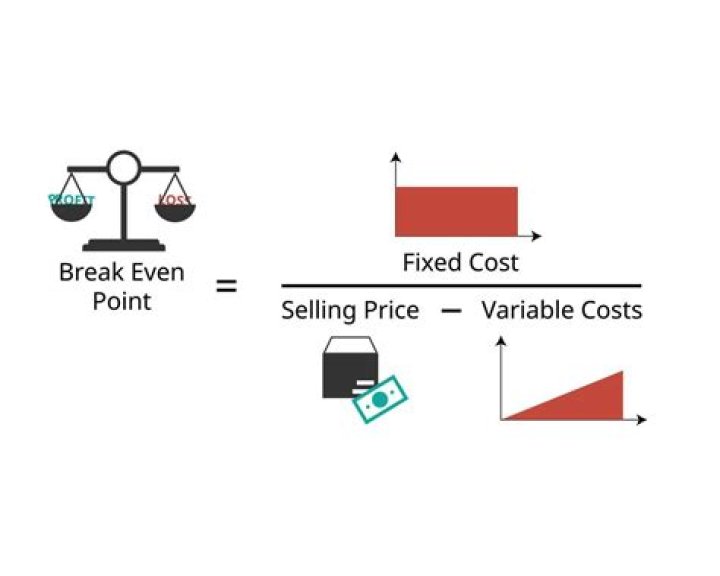

In accounting, the breakeven point is calculated by dividing the fixed costs of production by the price per unit minus the variable costs of production. The breakeven point is the level of production at which the costs of production equal the revenues for a product.

What happens to the break-even point in units of total fixed cost increases?

If fixed costs increase, the break-even point decreases. total revenue equals total cost. If variable cots per unit increase, then the breakeven point will decrease. If a company increases fixed costs, then the breakeven point will be lower.

How to calculate break even for fixed costs?

The formula for break even analysis is as follows: Break even quantity = Fixed costs / (Sales price per unit – Variable cost per unit) Fixed costs are costs that do not change with varying output (e.g., salary, rent, building machinery). Sales price per unit is the selling price (unit selling price) per unit.

How to calculate the break even point in units?

How to Calculate the Break-Even Point. Hub > Accounting. To calculate the break-even point in units use the formula: Break-Even point (units) = Fixed Costs ÷ (Sales price per unit – Variable costs per unit) or in sales dollars using the formula: Break-Even point (sales dollars) = Fixed Costs ÷ Contribution Margin. Here’s What We’ll Cover:

How is sales price per unit related to break even?

Sales price per unit is the selling price (unit selling price) per unit. Variable cost per unit is the variable costs incurred to create a unit. It is also helpful to note that sales price per unit minus variable cost per unit is the contribution margin Contribution Margin Contribution margin is a business’ sales revenue less its variable costs.

How to calculate break even point for Barbara’s factory?

First we need to calculate the break-even point per unit, so we will divide the $500,000 of fixed costs by the $200 contribution margin per unit ($500 – $300). As you can see, the Barbara’s factory will have to sell at least 2,500 units in order to cover it’s fixed and variable costs.