What is going concern principle with example?

Examples of Going Concern A state-owned company is in a tough financial situation and is struggling to pay its debt. The government gives the company a bailout and guarantees all payments to its creditors. The state-owned company is a going concern despite its poor financial position.

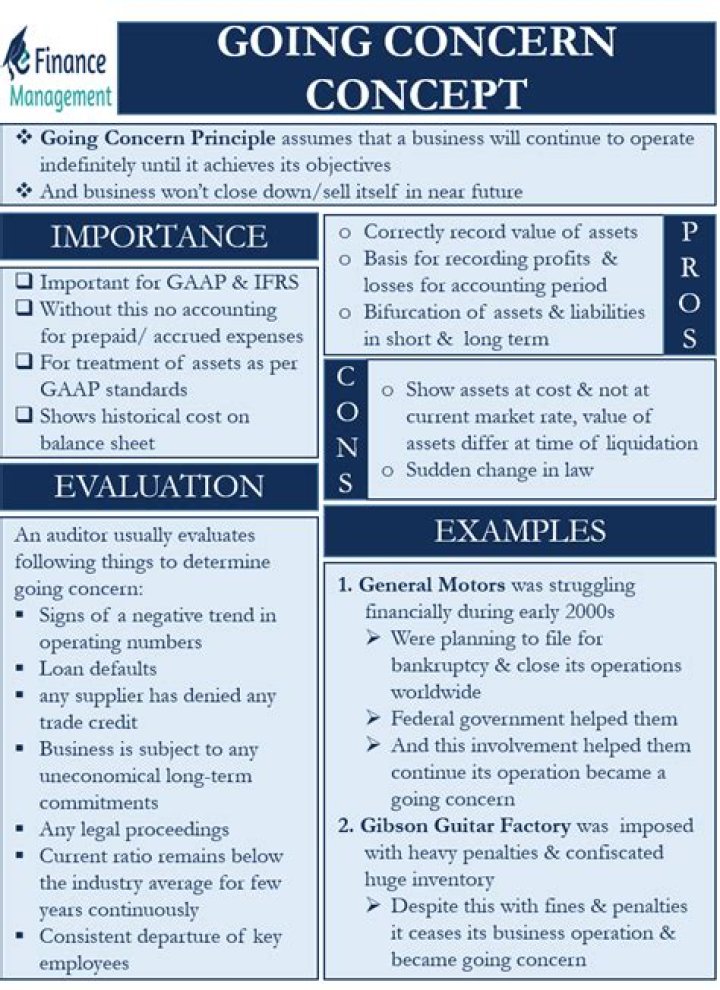

What is the purpose of the going concern principle?

As an accounting principle, the going concern principle serves as a guideline which allows readers of a business’s financial statements to assume that the business will continue to operate long enough to carry out its current obligations, objectives and commitments.

What are the exception of going concern concept?

If a company is a going concern (and therefore liquidation is not relevant), reporting its long term assets at cost is sufficient and there is no need to report the long term assets at their current values or liquidation values? (An exception to cost exists when a long term asset’s value has been impaired.)

How do you calculate going concern?

How to Assess Going-Concerns

- Current ratio: Divide current assets by current liabilities to get the current ratio.

- Debt ratio: Total liabilities divided by total assets provides the company’s debt ratio.

- Net income to net sales: This ratio measures how well the company is managing its expenses.

What is the difference between going concern and liquidating concern?

Going-concern value represents the monetary value that can reasonably be expected to be received from continuing business operations, and liquidation value represents the total sales value of all company-owned assets.

What is definition of going concern value?

Going concern value is a value that assumes the company will remain in business indefinitely and continue to be profitable. Going concern value is also known as total value. A company should always be considered a going concern unless there is a good reason to believe that it will be going out of business.

What is the concept of a going concern?

Going Concern Concept The going concern concept states that a business will continue its operations for the foreseeable future. This implies that the company will not be forced to discontinue its operations and liquidate its assets at extremely low costs.

How is the going concern principle used in accounting?

The going concern principle in accounting is much like your vacuum cleaner. You assume that your vacuum cleaner is operable because you have no evidence that it is broken. As an accountant, you might also assume that a business is a going concern (that is, in operation) unless you have evidence to the contrary.

What makes no sense without the going concern principle?

Some things in accounting would make no sense without the going concern principle. For example, if we expected a company to go out of business a few months from now, it would make no sense to record any long-term liabilities for that firm, because we wouldn’t expect the business to still be there to pay them.

When does an entity become a going concern?

However, generally accepted auditing standards (GAAS) do instruct an auditor regarding the consideration of an entity’s ability to continue as a going concern. The auditor evaluates an entity’s ability to continue as a going concern for a period not greater than one year following the date of the financial statements being audited.