What is inherent risk control risk and detection risk?

Detection risk occurs when an auditor fails to identify a material misstatement in a company’s financial statements. There are three types of audit risk: detection risk, inherent risk, and control risk. Auditors must implement correct audit procedures to limit detection risk.

What are the three types of audit risk?

There are three common types of audit risks, which are detection risks, control risks and inherent risks.

What is inherent risk in an audit?

Inherent risk is the risk posed by an error or omission in a financial statement due to a factor other than a failure of internal control. In a financial audit, inherent risk is most likely to occur when transactions are complex, or in situations that require a high degree of judgment in regard to financial estimates.

What is the meaning of audit risk?

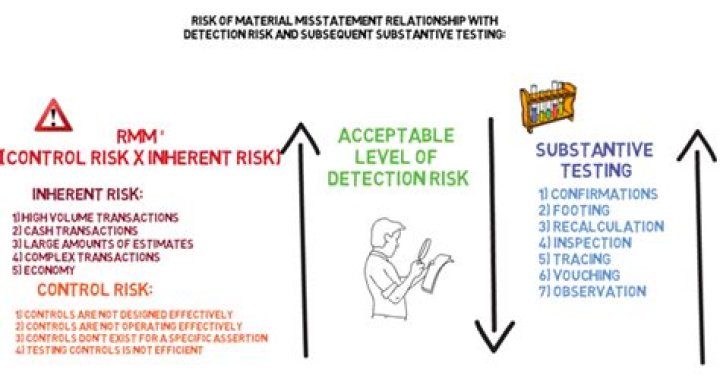

Audit risk is defined as ‘the risk that the auditor expresses an inappropriate audit opinion when the financial statements are materially misstated. Audit risk is a function of the risks of material misstatement and detection risk’.

How do you identify audit risks?

4 tips to identify audit client risks

- Don’t be afraid to ask questions.

- Know your client’s industry and their transaction cycles.

- Identify your client’s controls.

- Evaluate the design and implementation of your client’s controls.

- Tracy Harding, CPA, Principal, BerryDunn.

What are examples of inherent risks?

Inherent Risk Factors

- Susceptibility to theft or fraudulent reporting.

- Complex accounting or calculations.

- Accounting personnel’s knowledge and experience.

- Need for judgment.

- Difficulty in creating disclosures.

- Size and volume of accounts balance or transactions.

- Susceptibility to obsolescence.

- Prior year period adjustments.

How do you identify audit risk?

What are the methods of risk control?

Risk control methods include avoidance, loss prevention, loss reduction, separation, duplication, and diversification.

How do you determine inherent risk?

Inherent risk is assessed primarily by the auditor’s knowledge and judgment regarding the industry, the types of transactions occurring at a particular company and the assets that the company owns. Usually, an auditor assesses each audit area as either low, medium or high in inherent risk.

What is inherent risk in it?

Inherent risk represents the amount of risk that exists in the absence of controls.

What are the elements of audit risk?

There are three components of an audit risk from the viewpoint of the auditor — inherent risk, control risk and detection risk.

How do you identify inherent risks?

What are examples of inherent risk?

What are the 3 types of audit risk?

There are three common types of audit risks, which are detection risks, control risks and inherent risks. This means that the auditor fails to detect the misstatements and errors in the company’s financial statement, and as a result, they issue a wrong opinion on those statements.

Audit risk is defined as ‘the risk that the auditor expresses an inappropriate audit opinion when the financial statements are materially misstated. Audit risk is a function of the risks of material misstatement and detection risk’. control risk.

What are 3 types of auditing?

What Is an Audit?

- There are three main types of audits: external audits, internal audits, and Internal Revenue Service (IRS) audits.

- External audits are commonly performed by Certified Public Accounting (CPA) firms and result in an auditor’s opinion which is included in the audit report.

When to use inherent risk in an audit?

When conducting an audit or analyzing a business, the auditor or analyst tries to gain an understanding of the nature of the business while examining control risks and inherent risks. If inherent and control risks are considered to be high, an auditor can set the detection risk to an acceptably low level to keep…

How is inherent risk, control risk and detection risk calculated?

The control risk for the audit may therefore be considered as high. If inherent risk and control risk are assumed to be 60% each, detection risk has to be set at 27.8% in order to prevent the overall audit risk from exceeding 10%.

What are the different types of Audit Risks?

As mention above, inherent risks and control risks have come from clients whereas detection risks are control by auditors. All of these three risks are discussed below: Here is the formula: Audit Risks = Inherent risks * Control risks * Detection risks Let me clarify about the formula here.

How does detection risk affect an Audit Strategy?

Detection risk directly influences audit strategy. For example, if an audit requires a low detection risk to counter a high control risk, auditors may rely less on control testing and conduct extensive substantive procedures to form a valid audit opinion.