What is inland marine floater insurance?

Inland marine insurance is a “floater” policy, which simply means the coverage goes where the insured property goes. A small business that ships valuables, transports tools, or owns a truck with specialized equipment may need this policy. Read more about inland marine coverage.

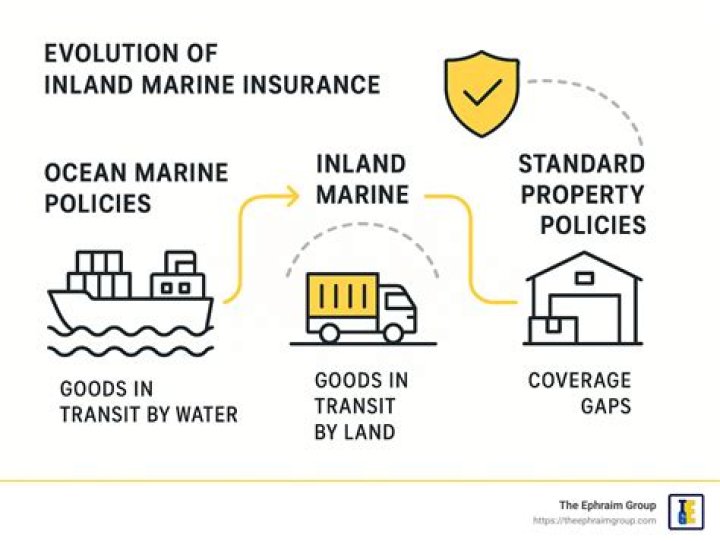

Why are inland marine policies called floaters?

Inland marine policies became known as “floaters” since the property to which coverage was originally extended was essentially “floating.” The coverage has grown to include property that just involves an element of transportation.

What types of property can usually be insured under an inland marine dealer policy?

Inland Marine Coverage — property insurance for property in transit over land, certain types of moveable property, instrumentalities of transportation (such as bridges, roads, and piers), instrumentalities of communication (such as television and radio towers), and legal liability exposures of bailees.

What does a floater cover in an insurance policy?

Floater insurance is a type of insurance policy that covers personal property that is easily movable and provides additional coverage over what normal insurance policies do not. Also known as a “personal property floater,” it can cover anything from jewelry and furs to expensive stereo equipment.

What are the six classes of property that can be covered under an inland marine policy?

Some types of property that can be covered by Inland Marine Insurance include:

- Property that is being moved or transported.

- Property you’re holding for someone else.

- Property installed in a vehicle.

- Property that moves from place to place.

- Fixed property that can be used for transportation or communication.

Does inland marine cover property in transit?

Inland marine insurance protects business property in transit, which is typically excluded from commercial property insurance.

How much does floater insurance cost?

What is the Cost of the Policy? A stand-alone Jewelry Policy costs between 1% to 2% of all the jewelry scheduled on the policy. For example, if you have $20,000 in scheduled jewelry on a policy you can expect to pay $200 to $400 per year.

What is the difference between a personal articles floater and a personal property floater?

In an Inland Marine policy, what is the difference between the Personal Articles Floater (PAF) and the Homeowners Scheduled Personal Property Endorsement? The PAF must have an appraisal and the Scheduled may not. The PAF provides more coverage than the Homeowners Scheduled Personal Property Endorsement.

Which inland marine coverage condition says that an insurer will settle?

Cards

Term What is a filed inland marine policy? Definition Filed coverages have standardized coverage forms Term Which inland marine coverage condition says that an insurer will settle with the actual owners of property involved in a loss? Definition Privilege to adjust with the owner What risks are covered under marine and inland transit cover?

This policy covers the risk of theft, piracy and damage to goods while loading or unloading. However, there are certain risks like strike, violence etc. against which an extra cover needs to be availed by the insured under special clauses of the policy.

What kind of insurance does a theatrical floater cover?

It also covers such risks as flood, collapse of bridges, vehicle derailment or damage, stranding and sinking of vessels, and aircraft crash. A theatrical floater is also referred to as a theatrical property floater. A theatrical floater does not cover buildings, furniture, and other items not directly used in a theatrical production.

Can a contractor get insurance for a floater?

For contractors, the property they rely on to complete their work can be compromised along the way. Most commercial property insurance policies provide little to no coverage for property once it has been removed from a contractor’s premises.

When do you need a commercial property floater?

Assuring protection against all such risks may require a commercial property floater. Many businesses which operate from a central headquarters require commercial property floaters to protect equipment routinely taken offsite.

How does coinsurance work in a property insurance policy?

A majority of property insurance policies contain a coinsurance provision. A coinsurance provision requires the insured to insure the covered property to a specified percentage of it’s full value, typically 80, 90 or 100 percent.