What is journal in accounting cycle?

A journal entry is a record of the business transactions in the accounting books of a business. A properly documented journal entry consists of the correct date, amounts to be debited and credited, description of the transaction and a unique reference number. A journal entry is the first step in the accounting cycle.

What are the phases in an accounting cycle?

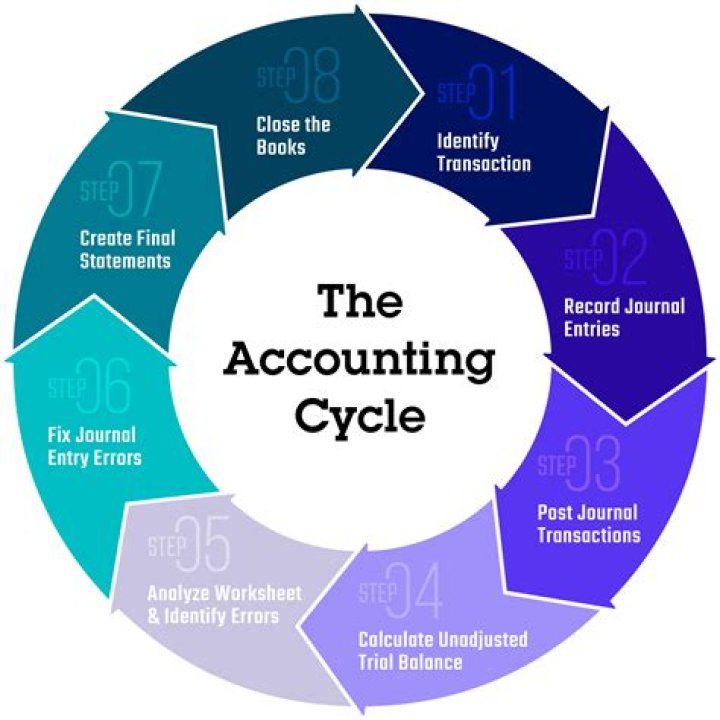

The eight steps of the accounting cycle are as follows: identifying transactions, recording transactions in a journal, posting, the unadjusted trial balance, the worksheet, adjusting journal entries, financial statements, and closing the books.

What are the 5 stages of accounting?

Explaining Accounting Cycle in Context Defining the accounting cycle with steps: (1) Financial transactions, (2)Journal entries, (3) Posting to the Ledger, (4) Trial Balance Period, and (5) Reporting Period with Financial Reporting and Auditing.

What is journaling in accounting?

A journal is a detailed account that records all the financial transactions of a business, to be used for the future reconciling of accounts and the transfer of information to other official accounting records, such as the general ledger.

Which is the second stage of the accounting cycle?

The second stage in the accounting cycle is posting entries from journal to the ledger account. Ledger is the principal book of accounting system. Whereas, journal is the original book of entry. General Ledger consists of numerous accounts in which transactions pertaining to these accounts are recorded.

What are journal entries in the accounting cycle?

Journal Entries Guide Journal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits). Without proper journal entries, companies’ financial statements would be inaccurate and a complete mess.

Which is the most important phase of accounting?

Accounting recorders include records of assets, liabilities, ledgers, journals and other supporting documents such as invoices and checks. The classifying phase of accounting involves sorting and grouping similar items under the designated name, category or account.

What are the categories in an accounting cycle?

All accounts are divided into five categories in order to record business transactions. These include assets, liabilities, capital, expenses/losses and income/gains. Posting involves the practice of transferring journal entries from the journal to the ledger.