What is loss on house property in income tax?

Loss from house property: When you own a self occupied house, since its GAV is Nil, claiming the deduction on home loan interest will result in a loss from house property. This loss can be adjusted against income from other heads.

What is loss from house property section 24?

Section 24 of the Income Tax Act lets homeowners claim a deduction of up to Rs. 2 lakhs (Rs. 1,50,000 if you are filing returns for last financial year) on their home loan interest if the owner or his family reside in the house property.

Can house property loss be set-off from salary income?

Loss from House property can be set off against income under any head. Business loss other than speculative business can be set off against any head of income except income from salary.

Is loss from house property allowed in new tax regime?

House property loss under the new tax regime In case of a self-occupied property, you cannot claim a deduction on interest for a housing loan under the new tax regime. In the new regime, you cannot set-off the loss arising from the house property due to excess of interest paid over the rental income.

How do you calculate loss on house property?

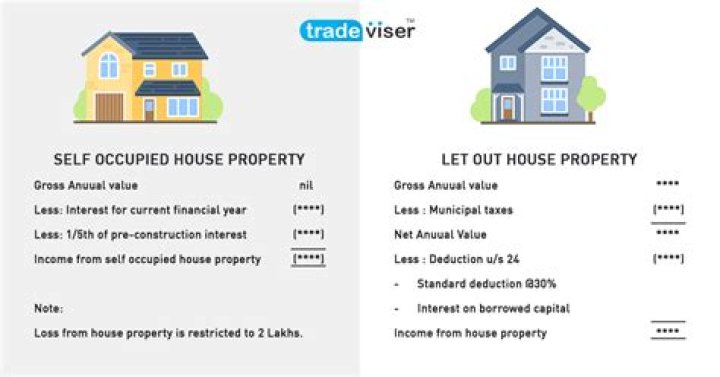

Loss from House Property: Income Tax Treatment

- Gross Annual Value (i.e. Actual Rent or Expected Rent, whichever is higher) xxx. (Less)

- Municipal and Other taxes paid to Local Authority. (xxx)

- Net Annual Value (1-2) xxx. (Less)

- Deductions allowed under Section 24. a. Statutory Deduction @ 30% of NAV. (xxx) b.

How many years loss from house property can be carried forward?

8 assessment years

Carry-forward of Loss from House Property Such Loss from House Property is allowed to be carried forward for a maximum of 8 assessment years. Such carry forward of Loss would be required to be shown in the Income Tax Return.

What is admissible loss from house property?

If the net result of computation of income under the head “House Property” is loss then such loss can be set-off against any other income upto Rs. 2 Lakh in any assessment year. However, the loss which couldn’t be set off can be carried forward for set-off in subsequent years.

What deductions are not allowed in new tax regime?

In the new tax regime, one will not get the deduction available in respect of EPF as well as standard deduction of Rs. 50000 for salaried class. These and other deductions such as those available against home loan, insurance premium will in the new tax regime not help you to lower your tax liability.

How the losses from house property can be set off and carried forward?

The total loss from house property can be adjusted with any other sources of income such as salary etc. In case you are not able to set-off the interest of Rs 2 lakh against any of income header, such surplus interest can be carried forward for eight assessment years.

What is the set off of loss from house property?

While computing the income (or loss) from the house property, the interest amount which is claimed as a deduction is known as ‘Deduction’ from house property income. The resultant figure (if in negative) is called Income (Loss) from House Property. When the resultant loss is adjusted with other income, the process is called ‘set-off of losses’.

Is the computed loss from house property beneficial?

The computed loss from house property is tax beneficial to an assessee. This is because the loss is allowed to be set-off against any other income of the assessee including salary income. Such a set-off of loss reduces the taxable income of the taxpayer which ultimately reduces the tax liability.

How is loss under head income from house property adjusted?

This loss can be adjusted against income from other heads. Note: When a property is let out, its gross annual value is the rental value of the property. The rental value must be higher than or equal to the reasonable rent of the property determined by the municipality. 3. Tax Deduction on Home Loans a.

How is income from let out property taxed?

Income from let out house property: In case if your property is let out, you will receive rent from your tenant (s). This rent income will be taxed as your income from house property. In short rental income received by the owner from letting out the house property will be taxed under income from house property.