What is minimum variance portfolio formula?

Understanding Portfolio Variance Portfolio variance is calculated by multiplying the squared weight of each security by its corresponding variance and adding twice the weighted average weight multiplied by the covariance of all individual security pairs.

Is the minimum variance portfolio the optimal portfolio?

Minimum variance weighted portfolios are optimal if all investments have the same expected return, while Maximum Diversification weighted portfolios are optimal if investments have the same Sharpe ratios.

What does it mean to have a minimum variance portfolio?

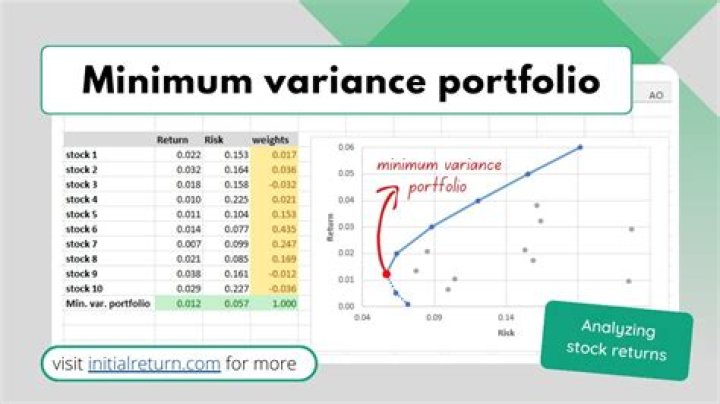

Minimum-variance portfolios are portfolios included in the investment opportunity set which have the minimum variance (i.e. minimum risk) at any particular level of expected return. Any portfolios to the left of the minimum-variance portfolio (at the same expected return) are not attainable, and any portfolio to the right is not optimal.

Which is the efficient part of the minimum variance curve?

Efficient Frontier. The portion of the minimum-variance curve that lies above and to the right of the global minimum variance portfolio is known as the Markowitz efficient frontier as it contains all portfolios that rational, risk-averse investors would choose.

Which is the optimal portfolio for diversification and risk?

Optimal Risky Portfolios Diversification and Portfolio Risk Portfolios of Two Risky Assets Asset Allocation with Stocks, Bonds, and Bills The Markowitz Portfolio Selection Model Optimal Portfolios with Restrictions on the Risk-Free Asset 3 DIVERSIFICATION AND PORTFOLIO RISK

Which is the optimal risk to variability ratio?

The Optimal Risky Portfolio with Two Risky Assets and a Risk-Free Asset. Thus the reward-to-variability ratio on the CAL that is supported by Portfolio B is SB = (9.5% – 5%)/11.7% = .38 which is higher than the reward-to-variability ratio of the CAL that we obtained using the minimum- variance portfolio and T-bills.