What is nonqualified deferred compensation income?

With a nonqualified deferred compensation (NQDC) plan, your employees can defer some of their pay until a later date. This type of deferred compensation plan typically pays out income after an employee leaves their job, like in retirement, for instance.

Are nonqualified deferred compensation plans a good idea?

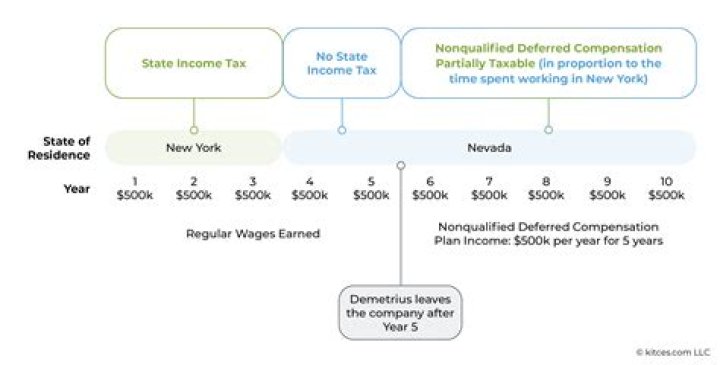

Are you working in a high-tax state but plan to retire in a state with low or no income tax? If so, a nonqualified deferred compensation plan could give you a greater tax benefit, as you avoid tax now at higher rates.

What are different types of nonqualified deferred compensation?

There are two main types of nonqualified deferred compensation plans from which small business owners may choose: supplemental executive retirement plans (SERPs) and deferred savings plans. These two options share several common characteristics, but there are also important differences between the two.

What is the advantage of nonqualified deferred compensation plans?

“Deferring this income provides one tax advantage: You don’t pay federal or state income tax on that portion of your compensation in the year you defer it (you pay only Social Security and Medicare taxes), so it has the potential to grow tax-deferred until you receive it.”

Is a non-qualified deferred compensation plan tax deductible?

Most employers implement “unfunded” NQDC plans in the US. Under a NQDC plan, employers can only deduct the benefit as the employee includes the benefit in taxable income. The deduction amount is the total amount included in the employee’s taxable compensation, which includes any earnings on the employer contributions.

Which of the following is a disadvantage of a non-qualified deferred compensation plan?

From the employer’s perspective, the biggest disadvantage of NQDC plans is that compensation contributed to the plan isn’t deductible until an employee actually receives it. Contributions to qualified plans are deductible when made. From the employee’s perspective, NQDC plans can be riskier than qualified plans.

How are non-qualified deferred compensation plans taxed?

Distributions to employees from nonqualified deferred compensation plans are considered wages subject to income tax upon distribution. Since nonqualified distributions are subject to income taxes, these amounts should be included in amounts reported on Form W-2 in Box 1, Wages, Tips, and Other Compensation.

What do you mean by non qualified deferred compensation?

Non-Qualified Deferred Compensation (NQDC) What Is Non-Qualified Deferred Compensation (NQDC) Non-Qualified Deferred Compensation is compensation that has been earned by an employee, but not yet received from their employer.

Can a company contribute to a deferred compensation plan?

Some NQDC plans only provide for employee elective contributions, permitting employees to elect to defer compensation earned in one year until a later time or event as stated in the plan. Other NQDC plans provide for employer-only or employee and employer contributions.

What’s the difference between NQDC and salary deferral?

The difference between the two kinds of plans lies in the way people use them and how the law views them. Through NQDC plans, employers can offer bonuses, salaries and other kinds of compensation. But instead of giving out this additional income right away, employers defer payment and give it out at a later date.

Can you withdraw from a deferred compensation plan without penalty?

Plan may permit in-service withdrawals without penalty after age 59½. Not generally. However, some plans allow you to choose a withdrawal upon a stated date or age. You would have to elect this option in advance or when the election is made to defer the compensation and the distribution would be subject to income tax.