What is normal loss?

Normal loss is the loss that occurs due to the nature of the goods consigned. Its nature is as follows: It occurs due to unavoidable reasons. It is due to natural causes such as losses due to evaporation, normal leakage, spoilage, breakdown, drying etc.

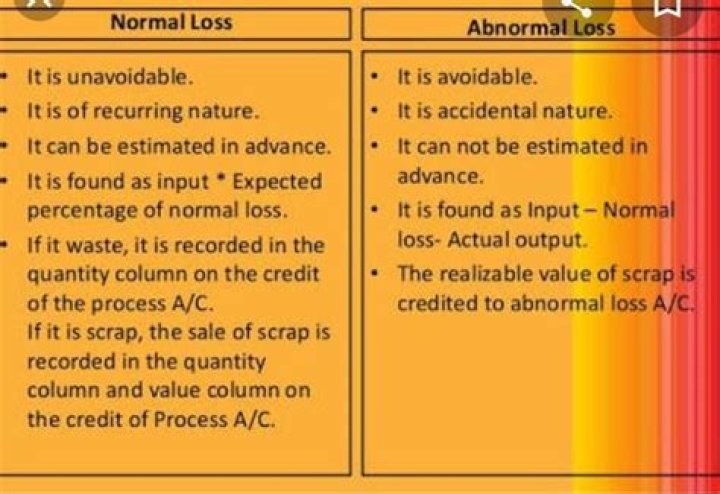

What is normal and abnormal loss in cost accounting?

Normal Loss is any loss which is incurred during the normal course of operation in the process. Abnormal Loss is a loss which happens accidently. These are not of a recurring nature and are not incurred during the normal course of operation in the process.

What is normal loss give some examples?

The normal loss means a loss which is inherited and can not be avoided. It should also be considered while valuing the closing stock. For example: If a certain amount of oranges are consigned, some of them will be destroyed in loading and unloading whereas some of them will not be in a state to be sold.

How do you calculate normal loss?

Normal loss in department subsequent to first

- Lost unit cost = [Cost from preceding department ÷ Good units] – Unit cost from preceding department before adjustment.

- Lost unit cost = (Lost units × Unit cost from preceding department before adjustment) ÷ Good units.

How is abnormal loss treated balance sheet?

The Abnormal Loss a/c has a debit balance and has to be closed by transferring the balance to the Profit & Loss a/c. Thus the Abnormal Loss a/c has to be credited. Transfer of a debit balance from one account to a second results in the second account being debited and the first account being credited.

How is abnormal loss treated?

Abnormal Loss Accounting The first step is to calculate the cost of goods that are lost. The consignment account is credited with this value and the abnormal loss account is debited. It is then transferred to the profit and loss account to arrive at the correct profit or loss of consignment.

Is abnormal loss shown in branch account?

Branch Profit and Loss Account: This account is credited with the amount of gross profit which is transferred from Branch Adjustment Account, Cost of surplus of stock or any revenue income and this account is debited with all branch expenses, depreciation, cost of abnormal loss of stock, etc.

Is abnormal loss an expense?

Accounting for an abnormal loss An abnormal loss is a cost to your business. It should therefore be treated as an expense and shown on your income statement.

What is the entry of abnormal loss?

Debit – Abnormal Loss a/c This would amount to brining the asset by name Abnormal Loss into usable condition. Thus, the expenditure should go into the value of the asset Abnormal Loss. The debit balance in the Abnormal Loss a/c reflects its value.

What is abnormal gain in cost accounting?

Abnormal gain arises because of an abnormal effective in the use of raw material or efficiency in performance so it is known as abnormal effective. Abnormal gain reduces the normal loss quantity so it comes in the form of profit to the industry. The value of an abnormal gain is assessed on the basis of production cost.

How do you account for abnormal gain?

Abnormal Gain – Accounting Treatment

- Actual Output Units. = Net Output Units + Abnormal Gain Units. = Gross Input units − Net Loss Units + Abnormal Gain Units. =

- Normal Cost of actual output. = Normal cost of normal output + value of Abnormal Gain Units. = Total Cost − Net Loss Realisation + value of Abnormal Gain Units. =

How is abnormal gain treated?

Accounting Treatment The value of abnormal gain is transferred to the debit side of the relevant process and ultimately closed by crediting it to the Costing Profit and Loss Account. Normal and abnormal loss concept are associated with processing costing.

What is an abnormal gain?

If the actual loss of a Process is less than that of expected loss then the difference between the two will be treated as abnormal gain. In another way we can define it as the difference between actual production and expected production.

The normal loss means a loss which is inherited and can not be avoided. It should also be considered while valuing the closing stock.

Normal loss cannot be avoided. Abnormal Loss is avoidable o account of precautions. CAUSES. This loss is due to nature of the goods such as evaporation, loss of weight, drying etc. This loss arises due to external reasons like loss by theft, fire, carelessness etc.

What is normal loss how is it treated in cost accounts?

Because process costs are allocated on expected output (not actual input), the normal loss is allowed for in the unit cost. Thus, normal loss is not allocated a cost: this is covered by Rule 3.

What is normal loss and abnormal loss?

The normal loss is considered to be 10%. The meaning of abnormal loss is any accidental loss to the consigned goods or loss caused by carelessness. Examples of such losses are loss by theft or loss by fire, earthquake, flood, accidents, war, loss in transit, etc. Such losses are considered abnormal.

What is abnormal loss how is it calculated?

Abnormal loss = {Normal cost at normal production / (Total output – normal loss units)} X Units of abnormal loss. Example : In process A 100 units of raw materials were introduced at a cost of Rs. 1000.

How do you account for abnormal loss?

Abnormal loss in quantity terms should be deducted from the gross input to obtain Net Output. Cost of abnormal loss units should be deducted from the total cost to obtain Net Cost of Output.

Why is abnormal loss added?

For calculating value of Goodwill based on the profits of the organisation, one has to consider only the Normal Profits. Therefore, any type of abnormal loss is added back and any type of abnormal gain is reduced from the given Profits to compute Normal Profits for the given period.

What is the treatment of abnormal loss?

The rate column is always to be obtained as a quotient using the relation Value Quantity . Abnormal loss in quantity terms should be deducted from the gross input to obtain Net Output. Cost of abnormal loss units should be deducted from the total cost to obtain Net Cost of Output.

What is an abnormal loss in cost accounting?

Ans. Abnormal loss in cost accounting is the loss that occurs over and above normal loss. In case of abnormal loss in process costing, it can be defined as the loss or spoilage of units in a processing department. Such a loss should not generally occur under efficient and normal working conditions.

How is value loss treated in normal loss accounting?

The value loss (difference between cost value and realisable value) of normal loss units is considered to be a normal cost and as such has to be borne by the good output. Thus we eliminate only the realisable value of normal loss units from the total cost by crediting it to the process a/c.

How to calculate normal loss in process costing?

In 2nd department, the per unit cost of 1.72 transferred in from preceding department must be adjusted for the lost units. The adjustment amount is $0.08 which can be worked out using one of the following two methods: In the above discussion, we have assumed that the normal loss is identified during the production process.

How are normal loss units and abnormal loss units valued?

For abnormal loss units cost and value are synonymous. Normal Loss is valued at a notional price which is its net realisable price. But abnormal loss is valued at cost. We consider realisation from abnormal loss units only on it being sold for a consideration.