What is not allowable for IRA?

The IRA deduction is phased out if you have between $66,000 and $76,000 in modified adjusted gross income (MAGI) as of 2021 if you’re single or filing as head of household. You’ll be entitled to less of a deduction if you earn $66,000 or more, and you’re not allowed a deduction at all if your MAGI is over $76,000.

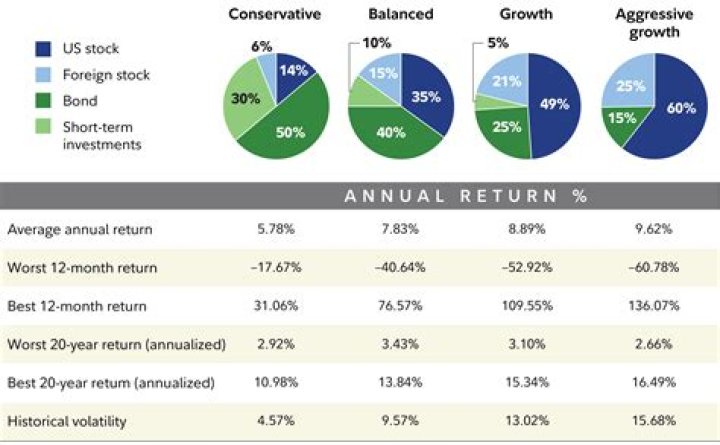

Can you lose money in IRAs?

An IRA is a type of tax-advantaged investment account that may help individuals plan and save for retirement. IRAs permit a wide range of investments, but—as with any volatile investment—individuals might lose money in an IRA, if their investments are dinged by market highs and lows.

What does it mean to have an IRA?

What is an IRA? IRA stands for Individual Retirement Account, and it’s basically a savings account with big tax breaks, making it an ideal way to sock away cash for your retirement. A lot of people mistakenly think an IRA itself is an investment – but it’s just the basket in which you keep stocks, bonds, mutual funds and other assets.

How are IRAS different from other financial assets?

Here are 6 significant differences between IRAs and other financial assets: Unless payable to an estate, IRAs do not pass through the will. Your IRA account has a beneficiary, who will receive your IRA at death, regardless of what you state in your will or living trust. Unless payable to an estate, IRAs are not subject to probate.

Where does the income from an IRA come from?

Income earned may come from different sources such as: Employment. Trade, Business, Profession or Vocation. Property or Investments. Other Sources (e.g. annuities, royalties, winnings or estate or trust income)

What happens to an IRA in a will?

Unless payable to an estate, IRAs do not pass through the will. Your IRA account has a beneficiary, who will receive your IRA at death, regardless of what you state in your will or living trust. Unless payable to an estate, IRAs are not subject to probate. This can be a significant time and cost savings in states where probate is arduous.