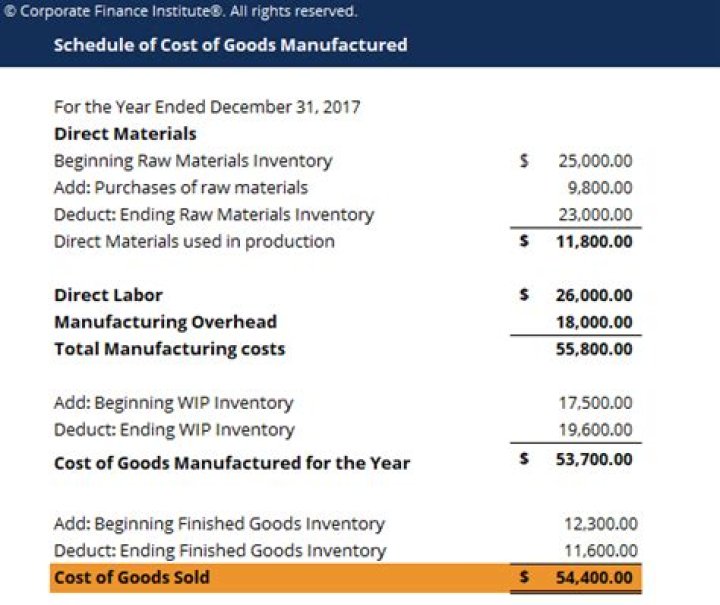

What is schedule of cost of goods manufactured?

The cost of goods manufactured schedule reports the total manufacturing costs for the period that were added to work‐in‐process, and adjusts these costs for the change in the work‐in‐process inventory account to calculate the cost of goods manufactured. …

What is the difference between COGM and COGS?

Cost of goods manufactured are the production costs incurred on finished goods produced in a specific accounting period. Cost of goods sold are the production costs incurred on goods actually sold in a specific accounting period.

Is cost of goods sold the same as cost of goods manufactured?

The cost of goods manufactured is composed of material and production costs, process costs and overhead (such as material and production overhead). The cost of goods sold consists of the cost of goods manufactured together with sales and administration overhead costs.

How to calculate total cost of goods manufactured?

Total Manufacturing Cost is calculated using the formula given below Total Manufacturing Cost = Direct Labor Cost + Direct Material Cost + Factory Overhead Total Manufacturing Cost = $1.50 million + $2.50 million + $0.80 million Total Manufacturing Cost = $4.80 million

What does cogm stand for in manufacturing category?

COGM stands for the cost of goods manufactured. It’s a measure of the true cost of a manufactured item, including labor and overhead. It also takes into account the work in progress inventory. How to calculate cost of goods manufactured? First, determine the costs. Calculate the material and direct labor costs associated with production.

What do you mean by cost of goods sold?

Cost of goods sold (COGS) is the cost of selling products, in other words the cost of finished inventory ready for sale. If we get more specific; finished inventory is any type of finished product, goods or services, that is ready to be delivered to the customer.

How is raw materials inventory used to calculate cogm?

In order to determine the actual direct materials used by the company for production, we must consider the Raw Materials Inventory T-account. Raw materials inventory refers to the inventory of materials that are waiting to be used in production.