What is Section 481 A depreciation adjustment?

What is a 481(a) Adjustment? Under current IRS rules, the calculation of depreciation or repair deductions for prior years can be recomputed, and a one-time catch-up adjustment (i.e. IRC §481(a) adjustment) is allowed in the current tax year for missed deductions.

What is a positive 481 adjustment?

Spread Periods for IRC 481(a) Adjustments. A net positive IRC 481(a) adjustment increases income and is often referred to as a “government-favorable” adjustment. A net negative IRC 481(a) adjustment decreases income and may be referred to as a “taxpayer-favorable” adjustment.

Is 481 a adjustment permanent or temporary?

The IRC section 481-a adjustment period in general, is four years, beginning with the year of change for both positive and negative adjustments.

How do I change from IRS to cash accrual?

If you’ve chosen cash and now you need to switch, you’ll need Internal Revenue Service approval. To determine if you have to change, add the gross receipts for the most recent tax year to the previous two years and divide by three: As of 2012, if the average exceeds $5 million, you have to switch to accrual.

How do you correct depreciation not taken?

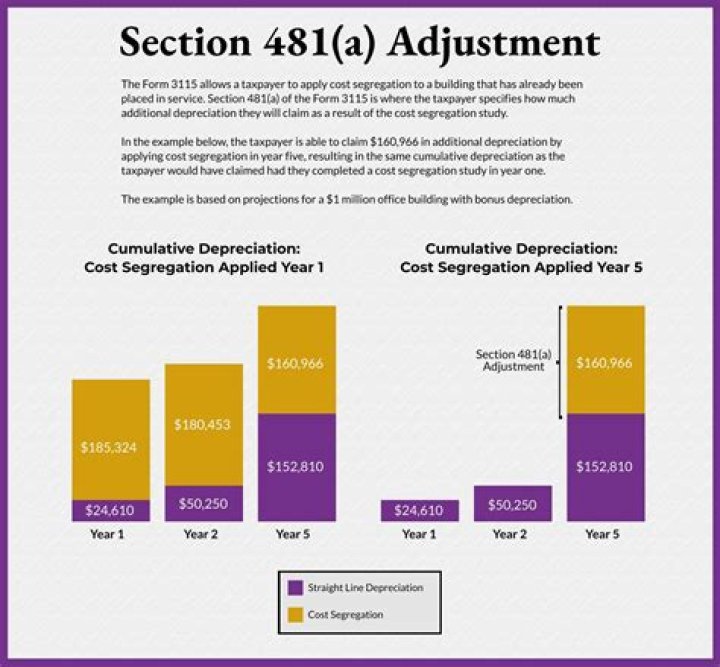

Form 3115, Change in Accounting Method, is used to correct most other depreciation errors, including the omission of depreciation. If you forget to take depreciation on an asset, the IRS treats this as the adoption of an incorrect method of accounting, which may only be corrected by filing Form 3115.

Can you switch depreciation methods?

Taxpayers can request an automatic method change for depreciation and amortization if the requirements are met to do so. Taxpayers may change from an impermissible method of accounting to a permissible method of accounting or from one permissible method of accounting to another permissible method of accounting.

What is Section 263 A?

What is Section 263A? Section 263A, often referred to as the Uniform Capitalization rules or UNICAP, requires taxpayers to capitalize direct and indirect costs properly allocable to real or tangible personal property produced or acquired for resale by the taxpayer.

Who has to file a Schedule M-3?

Any entity that files Form 1065 must file Schedule M-3 (Form 1065) if any of the following is true. The amount of total assets at the end of the tax year reported on Schedule L, line 14, column (d), is equal to $10 million or more. The amount of adjusted total assets for the tax year is equal to $10 million or more.

Is m-3 required?

The Schedule M-3 reporting requirement has been in place since 2004. It requires corporate and partnership entities that report assets of $10 million or more on their Schedule L balance sheet to reconcile taxable income or loss with financial statement income or loss.

When to make an adjustment under Section 481?

Section 481 provides that where a taxpayer’s taxable income for a tax year is computed under a method of accounting different from that previously used, an adjustment will be made to prevent amounts from being duplicated or omitted solely by reason of the change in accounting method.

What to do with 481a change in accounting method?

The company files a Form 3115 Change in Accounting Method, and calculates how much they will be underreporting revenue due to the change. Since they are under-reported, they must add the under-reported amount on Line 10 of Year Two. But if it is over $50,000, they may spread it out over four years (the year of the change plus three more years).

How many taxable years are there for IRC 481 ( a )?

The IRC 481 (a) adjustment period is one taxable year for a net negative adjustment and, in general, is four taxable years for a net positive adjustment for an accounting method change. If the taxpayer is under examination, the IRC 481 (a) adjustment period is two taxable years unless the taxpayer meets one of the exceptions.

What is the spread period for Section 481?

According to tax research service Thomson Reuters CheckPoint, “Under the new procedures for filing a Form 3115 for tax year 2015 and forward, the four-year spread period generally applicable to a positive Section 481 (a) adjustment has been modified as De minimis § 481 (a) adjustment amount increased.