What is significant accounting estimates?

In determining the carrying amounts of certain assets and liabilities, the Group makes assumptions of the effects of uncertain future events on those assets and liabilities at the balance sheet date.

Who is responsible for accounting estimates within the financial statements?

Management

03 Management is responsible for making the accounting estimates in- cluded in the financial statements. Estimates are based on subjective as well as objective factors and, as a result, judgment is required to estimate an amount at the date of the financial statements.

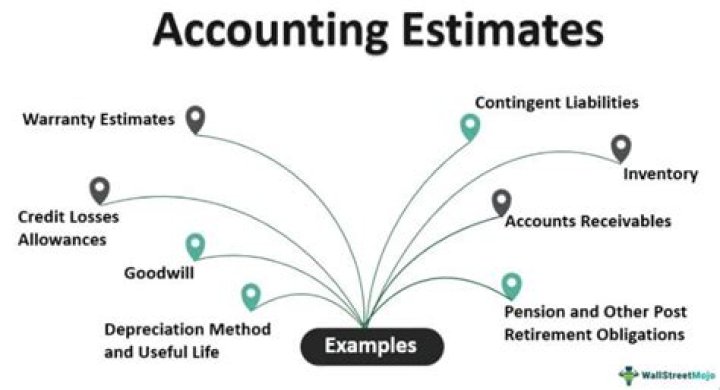

What is accounting estimate example?

Examples of accounting estimates include net realizable values of inventory and accounts receivable, property and casualty insurance loss reserves, revenues from contracts accounted for by the percentage-of-completion method, and pension and warranty expenses.

What are changes in accounting estimates?

A change in accounting estimate is an adjustment of the carrying amount of an asset or liability, or related expense, resulting from reassessing the expected future benefits and obligations associated with that asset or liability.

What is the difference between accounting policy and accounting estimate?

The difference between an accounting policy and an accounting estimate is that changes in estimates are recognized prospectively, while changes in policies are applied retrospectively.

How do you estimate financial statements?

Determine the operating margin of the business. This is the amount of each dollar that the business made in revenue that represents profit. Divide the total income that the business received by the net revenues and multiply by 100 to express the operating margin as a percentage.

How do you estimate an audit?

How Accounting Estimates are Audited

- Testing management’s process. Auditors evaluate the reasonableness and consistency of management’s assumptions, as well as test whether the underlying data is complete, accurate, and relevant.

- Developing an independent estimate.

- Reviewing subsequent events or transactions.

What method is used to account for a change in accounting estimate?

The rationale for a change of depreciation method to be treated as a change in accounting estimate is that: changing depreciation method is done to reflect changes in estimated future benefits.

How do you disclose change in accounting estimate?

Disclose: the nature and amount of a change in an accounting estimate that has an effect in the current period or is expected to have an effect in future periods. if the amount of the effect in future periods is not disclosed because estimating it is impracticable, an entity shall disclose that fact. [IAS 8.39-40]

What are its effect on the financial statements?

Financial statements can have a drastic effect on the stock price of a company. If information is presented in a financial statement that is better or worse than expected, it can send the stock price up or down. Investors often use financial ratios based on information from the financial statements to make assumptions.

What is audit uncertainty estimation?

Estimation uncertainty is ‘The susceptibility of an accounting estimate and related disclosures to an inherent lack of precision in its measurement’. The greater the estimation uncertainty, the more the client will need to explore the effect of different models and assumptions to make an appropriate estimate.

How do you identify change in accounting policy?

Following must be disclosed in the financial statements of the accounting period in which a change in accounting policy is implemented:

- Title of IFRS.

- Nature of change in accounting policy.

- Reasons for change in accounting policy.

- Amount of adjustments in current and prior period presented.