What is tax loss carryforward?

A tax loss carryforward (or carryover) is a provision that allows a taxpayer to move a tax loss to future years to offset a profit. The tax loss carryforward can be claimed by an individual or a business to reduce any future tax payments.

Which of the following could require Interperiod tax allocation?

require interperiod tax allocation? Unearned service contract revenue. Unearned service contract revenue creates a temporary difference as it would be included in income for tax purposes but would not be recognized in pretax accounting income as revenue until it is earned.

How is loss carried forward calculated?

Create a line to calculate the loss used in the period with a formula stating that “if the current period has taxable income, reduce it by the lesser of the taxable income in the period and the remaining balance in the TLCF. Create a closing balance line equal to the subtotal less any loss used in the period.

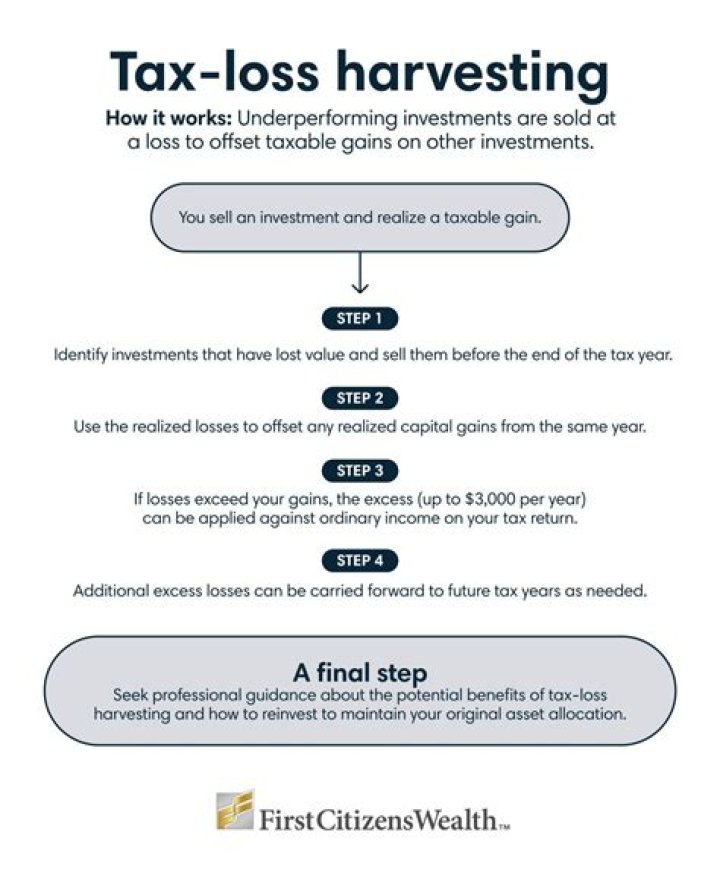

How do you carry over losses on taxes?

Carry over net losses of more than $3,000 to next year’s return. You can carry over capital losses indefinitely. Figure your allowable capital loss on Schedule D and enter it on Form 1040, Line 13. If you have an unused prior-year loss, you can subtract it from this year’s net capital gains.

How much of a stock loss is tax deductible?

Deducting and Writing Off Investment Losses You can write off up to $3,000 worth of short-term stock losses in any given year. Stocks you hold more than a year are long-term stocks. If you lose money on these, you count this as a long-term investment loss tax deduction.

How to recognize tax benefits due to a loss carryforward?

Recognition of tax benefits in the loss year due to a loss carryforward requires: The establishment of a deferred tax asset. Recognizing a valuation allowance for a deferred tax asset requires that a company: Consider all positive and negative information in determining the need for a valuation allowance. Uncertain tax positions…(1-4) 1. Only.

What should the current amount of deferred tax liability be?

The current amount of a deferred tax liability should generally be: based on the classification of the related asset or liability for financial reporting purposes. All of the following are procedures for the computation of deferred income taxes except to:

When is revenue deferred for financial reporting purposes?

A revenue is deferred for tax purposes but not for financial reporting purposes. 3. An expense is deferred for financial reporting purposes but not for tax purposes. A major distinction between temporary and permanent differences is: