What is the basis in a 1031 exchange?

The basis of property acquired in a Section 1031 exchange is the basis of the property given up with some adjustments. This transfer of basis from the relinquished to the replacement property preserves the deferred gain for later recognition.

What is the basis of property received in a fully nontaxable exchange?

If you trade property in a nontaxable exchange and pay money, the basis of the property received is the basis of the property exchanged increased by the money paid.

How do you calculate adjusted basis?

The adjusted basis is calculated by taking the original cost, adding the cost for improvements and related expenses and subtracting any deductions taken for depreciation and depletion.

What is the basis of exchange?

Exchange Basis means, as at any time, the number of Common Shares or other classes of shares or securities which a Warrantholder is entitled to receive upon the exercise of the rights attached to the Warrants pursuant to the provisions of this Indenture; Sample 2. Sample 3.

How is the basis of a like kind exchange calculated?

If the replacement property costs more than the net sales proceeds from the sale of the relinquished property, the excess amount is added to its basis. Another way to calculate the new basis is to take the cost of the replacement property and subtract the gain that is deferred in the like-kind exchange.

How does depreciation work in a like-kind exchange?

The first method separates the replacement property into two components for depreciation: the basis of the original or relinquished property; and the additional or excess basis from the exchange. The treatment varies based on the method and recovery period of the replacement property in comparison to the original property.

What are the regulations for like kind exchanges?

Recently, the IRS issued proposed regulations, which include a definition of real property to reflect the TCJA changes made for like-kind exchanges. These proposed regulations also provide guidance related to a taxpayer’s receipt of personal property incidental to the real property received (replacement property) in an exchange.

Can a like kind exchange defer capital gains?

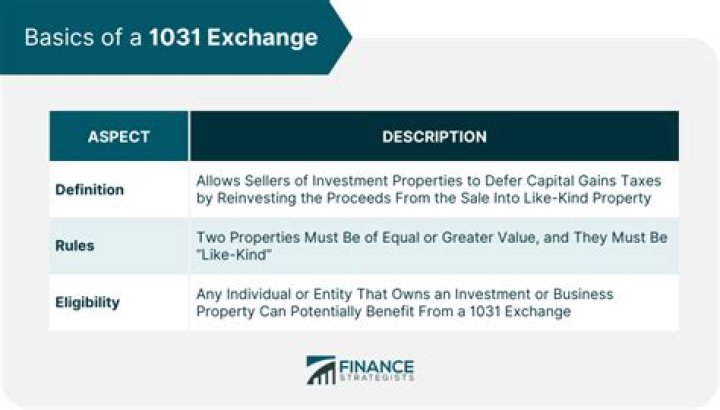

If you exchange real property used for business or held as investments, you can use an IRS-allowed technique known as a like-kind exchange to defer paying capital gains taxes and hold all your equity. In like-kind exchange, the money from a property sale is reinvested in another property.