What is the basis of assets distributed to a shareholder in liquidation?

The shareholder’s basis in assets received is their FMV at the time of the distribution. Basis is not affected by the shareholder’s assuming corporate liabilities or receiving corporate property that is subject to a liability (Sec. 334(a); see also Ford).

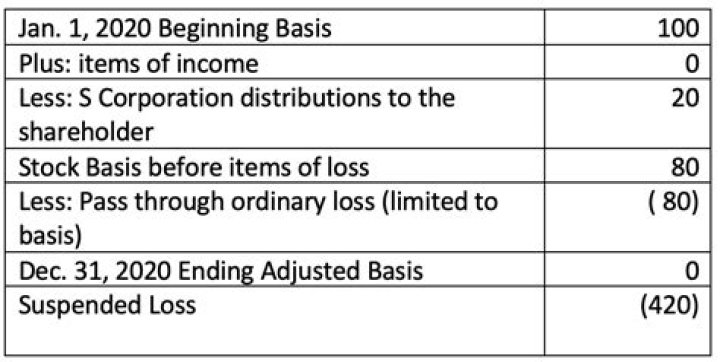

How does S Corp track shareholder basis?

In computing stock basis, the shareholder starts with their initial capital contribution to the S corporation or the initial cost of the stock they purchased (the same as a C corporation). That amount is then increased and/or decreased based on the pass-through amounts from the S corporation.

What is a liquidating distribution from S corporation?

The amount that a shareholder receives in a liquidating distribution is treated as full payment in exchange for the shareholder’s S corporation stock. In other words, if the S corporation is making a liquidating distribution, the shareholder is treated as having sold her stock for the amount of the distribution.

Do liquidating distributions reduce basis?

In either a liquidating or a nonliquidating distribution, a distribution of cash to the shareholder will only decrease the shareholder’s stock basis by the amount of cash distributed.

What happens when an S-Corp terminates?

When an entity loses its S corporation status, the entity becomes treated for U.S. federal tax purposes as a C corporation. In general, the S corporation’s tax year is deemed to end the day before the failure to adhere occurs and the C corporation’s tax year begins on the day of the failure to adhere.

How is a corporation affected when it distributes appreciated property to a shareholder?

If an S corporation distributes appreciated property to its shareholders, the difference between the fair market value and the property’s basis will result in a gain that will be passed through to the shareholders. In that case the gain is income to the other shareholders as well, based on share ownership.

What is the capital loss for liquidation of a LLC?

V has a $4,000 capital loss on the liquidating distribution, computed as shown in the exhibit below. Under the general distribution rules, V can allocate only $6,000 of basis to the distributed inventory—its adjusted basis to the LLC (Sec. 732 (c) (1)).

What are the rules for liquidation of a S corporation?

Liquidating distributions are not governed by the normal S corporation distribution rules. Instead, liquidation of an S corporation is governed by the same rules that apply to liquidation of a C corporation.

Are there exceptions to SEC 332 ( C ) for liquidating corporations?

There are exceptions under Sec. 332 (c) if the liquidating corporation is a regulated investment company or a real estate investment trust.

Can a gain be recognized on a liquidation of a LLC?

Possibility of Gain or Loss Recognition. Gain is recognized by a member in an LLC classified as a partnership on the receipt of a liquidating distribution to the extent money is distributed in excess of the distributee member’s basis in his or her LLC interest (see Sec. 731(a)(1)).