What is the closing journal entry for sales return?

The journal entries to close revenue accounts are to debit the revenue account and credit income summary, which is also a temporary account used for the closing process. The journal entries to close expense accounts are to credit the expense account and debit income summary.

How do you record closing entries for revenue?

Closing the revenue accounts—transferring the credit balances in the revenue accounts to a clearing account called Income Summary. Closing the expense accounts—transferring the debit balances in the expense accounts to a clearing account called Income Summary.

How do you close a sales returns account?

To close Sales, it must be debited with a corresponding credit to the income summary. Sales Discounts and Sales Returns and Allowances are both contra revenue accounts so each has a normal debit balance. Cost of Goods Sold has a normal debit balance because it is an expense.

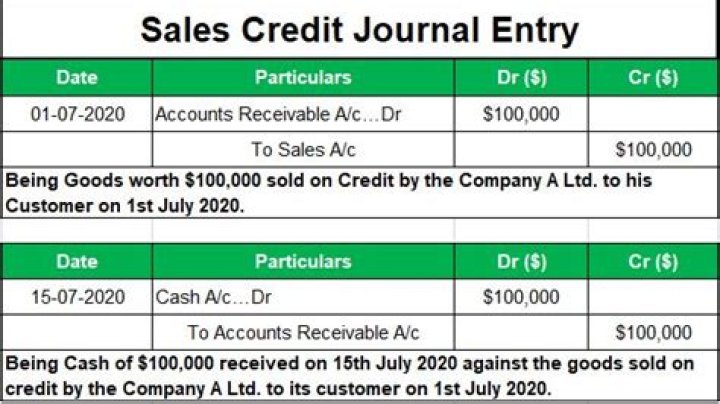

What is sales return journal entry?

Sales Return in terms of payroll journal entry can be defined as that the one which shall be used to account for the customer returns in the books of account or to account for when there is a return of goods sold by the customer due to defect goods sold, or misfit in requirement of the customer, etc.

What are closing journal entries?

A closing entry is a journal entry made at the end of the accounting period. It involves shifting data from temporary accounts on the income statement to permanent accounts on the balance sheet. All income statement balances are eventually transferred to retained earnings.

Do you close out sales returns and allowances?

To close revenue accounts with credit balances. 2. Close contra-revenue accounts and expense accounts with debit balances. We will close sales discounts, sales returns and allowances, cost of goods sold, and all other operating and nonoperating expenses.

How is sales return recorded in a journal entry?

In this case, the company provides an allowance to customers as compensation and the customers do not need to return goods. Hence, there is no impact on inventory and cost of goods sold transaction. So, only sales return account and its related credit size are recorded in the journal entry.

How does a closing journal entry get credited?

Closing Journal Entries Process. If a temporary account has a debit balance it is credited to bring it to zero, and the retained earnings account is credited to balance the closing entry. Likewise, if a temporary account has a credit balance, it is debited to bring it to zero and the retained earnings account is credited.

What should I add to my sales journal entry?

If your business deals with inventory, your sales journal entries are going to get a little more complex. But don’t panic: you’ll just need to add in two additional accounts to reflect your changes in inventory. When you sell a good to a customer, you’re getting rid of inventory.

When do you use reverse of journal entries?

Thus, for these transactions of returns, reverse of the journal entries recorded at the time of making the purchase or sale as the case may be sounds rational or convenient. In trying to understand the transactions of purchase returns and sales returns, please consider only credit transactions of purchase and sale.