What is the default rate on loans?

The default rate is the percentage of all outstanding loans that a lender has written off as unpaid after a prolonged period of missed payments. The term default rate–also called penalty rate–may also refer to the higher interest rate imposed on a borrower who has missed regular payments on a loan.

What are the current mortgage default rates?

For the first time since March 2020, the nation’s overall mortgage delinquency rate decreased from the year before. Early-stage delinquencies (30 to 59 days past due): 1%, down from 4.2% in April 2020. · Adverse delinquency (60 to 89 days past due): 0.3%, down from 0.7% in April 2020.

What is the Consumer Credit Index?

The S&P/Experian Consumer Credit Default Indices are designed to measure the balance-weighted proportion of consumer credit accounts which go into default each month.

What is the current delinquency rate?

The Federal Reserve System (FRS) provides public data on delinquency rates quarterly across the U.S. financial market. As of the fourth quarter of 2018, the total delinquency rate from loans and leases at commercial banks was 1.79%. Residential real estate loans reported the highest delinquency rate at 2.83%.

How is loan default interest calculated?

Default interest charges are calculated by multiplying the amount of arrears at the end of the day by the Daily Default Interest rate. The Daily Default Interest rate is calculated by dividing the Annual Default Interest rate by 365 to give a daily rate.

How is the default rate calculated?

The constant default rate (CDR) is calculated as follows: Take the number of new defaults during a period and divide by the non-defaulted pool balance at the start of that period.

What is a default mortgage?

A mortgage default arises when a borrower fails to make monthly payments to their principal balance or interest on a home loan. Yet, defaulting can also occur with credit card and student loans. A mortgage default can cause a borrower to lose their house and damage their credit score.

Will forbearance affect refinance?

Forbearance programs accomplished their goal of averting a foreclosure crisis, but the program carries a notable downside: If you’re not making payments, you’re not eligible to refinance your mortgage.

What do you need to know about default rates?

Key Takeaways 1 The default rate is the percentage of all outstanding loans that a lender has written off after a prolonged period of… 2 A loan is typically declared in default if payment is 270 days late. 3 Default rates are an important statistical measure used by economists to assess the overall health of the economy. More …

What does it mean when a loan is in default?

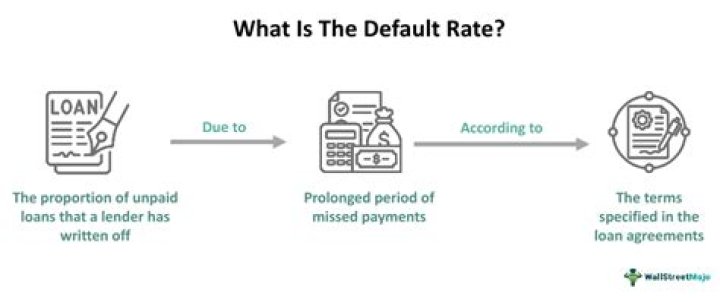

The default rate is the rate of all loans issued by a lender or financial institution that is left unpaid by the borrower and declared to be in default. The lending institution will write off the entire value of defaulted loans, removing it from the books altogether.

What’s the current default rate on a first mortgage?

The S&P/Experian Consumer Credit Default Composite Index is the most comprehensive of these indexes because it includes data on both first and second mortgages, auto loans, and bank credit cards. As of January 2020, the S&P/Experian Consumer Credit Default Composite Index reported a default rate of 1.02%.

How is the default rate for a student loan calculated?

The timeframe for default may vary depending on the type of loan. For student loans, default is approximately 270 days or nine months that no payments have been received. The default rate is calculated using the following formula: Default rates are important for lending institutions to measure their risk from borrowers.