What is the difference between cost of goods manufactured and cost of goods sold?

The cost of goods manufactured is composed of material and production costs, process costs and overhead (such as material and production overhead). The cost of goods sold consists of the cost of goods manufactured together with sales and administration overhead costs.

How do you calculate cost of goods manufactured in accounting?

The formula and format for presenting the cost of goods manufactured is:

- The cost of the direct materials used.

- PLUS the cost of the direct labor used.

- PLUS the cost of manufacturing overhead assigned.

- EQUALS = the manufacturing costs incurred in the current accounting period.

What is the importance of the cost of goods manufactured?

The cost of goods manufactured is important because it gives management a general idea of overall production costs and whether these costs are too high or too low. By better understanding the expenses of goods manufactured, the company can make adjustments to maximize overall profitability.

What should be included in COGS?

Cost of goods sold (COGS) is the cost of acquiring or manufacturing the products that a company sells during a period, so the only costs included in the measure are those that are directly tied to the production of the products, including the cost of labor, materials, and manufacturing overhead.

Is COGS a credit or debit account?

Cost of Goods Sold is an EXPENSE item with a normal debit balance (debit to increase and credit to decrease).

How do you find cost of goods sold from cost of goods manufactured?

To compute cost of goods sold, start with the cost of beginning inventory of finished goods, add the cost of goods manufactured, and then subtract the cost of ending inventory of finished goods. You have $19,500 in cost of goods sold, an amount that goes right to the income statement.

Do product costs become cost of goods sold?

In short, any costs incurred in the process of acquiring or manufacturing a product are considered product costs. When products are sold, the product costs become part of costs of goods sold as shown in the income statement.

What is difference between sales and cost of goods sold?

Sales is the monetary value of income earned by an entity by selling its products and/or services. Cost of goods sold is the sum total of all expenses incurred by the entity to produce the goods it has sold.

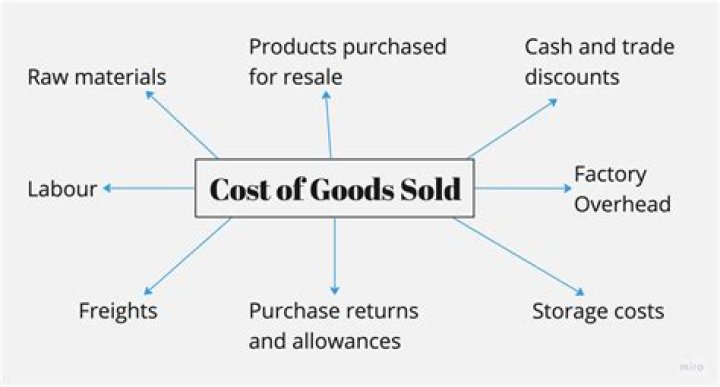

What makes up the cost of goods sold?

Cost of goods sold (COGS) refers to the direct costs attributable to the production of the goods sold in a company. This amount includes the cost of the materials used in creating the good along with the direct labor costs used to produce the good.

How to calculate cost of goods sold ( COGS )?

Stage IV: Calculate The Cost of Goods Sold 1 (1) COGS = cost of goods production + the initial inventory – inventory end 2 (2) COGS = 1.15 billion 400 million – 200 million + 3 (3) COGS = 1.35 billion.

What is the definition of cost of production?

The answer is: 11 December 2015 DEFINITION of ‘Production Cost’ A cost incurred by a business when manufacturing a good or producing a service. Production costs combine raw material and labor. To figure out the cost of production per unit, the cost of production is divided by the number of units produced.

What’s the difference between cogs and LIFO cost of goods sold?

The first two are self-explanatory. Under FIFO, COGS consists of earlier costs, whereas under LIFO, COGS consists of later costs. For example, assume that a company purchased materials to produce four units of their goods.