What is the difference between earnings management and creative accounting?

Earnings management (EM) is a subset of creative accounting (CA). That is EM focuses on manipulating earnings through accruals and deferrals whereas CA can be EM plus fictitious transactions like Enron did. EM and CA have their own literature with some overlap.

What is meant by earnings management?

Earnings management refers to a company’s deliberate use of accounting techniques to make its financial reports look better. Earnings management can occur when a company feels pressured to manipulate earnings in order to match a pre-determined target.

What is the difference between earnings management and earnings manipulation?

[6], accounting practices that violate the GAAP and IAS are called earning manipulation and fraudulent accounting. Moreover, if management uses their discretions which do not violate the GAAP or IFRS then it is called earning management. [9] the aggressive use of discretionary accrual causes earning manipulation.

Is earnings management good or bad?

While managers generally view earnings management as unethical, managers who have worked at companies with cultures characterized by fraudulent financial reporting believe earnings management is more morally right and culturally acceptable than managers who haven’t worked in such an environment.

How is earnings management done?

An earnings management strategy uses accounting methods to present an excessively positive view of a company’s financial positions, inflating earnings. Earnings management is used by companies to flatten out earnings variations and present profits that are consistent each quarter or year.

What are some of the way to manage earning?

Accounting Methods Used to Manage Earnings

- Cost flow assumptions. Choosing a cost flow assumption can affect profitability.

- Accrual accounting vs. cash basis accounting.

- Deferred tax estimates.

- Depreciation method.

- Capitalization practices.

- Acquisitions.

- Goodwill.

- The preparation of the statement of cash flows.

What are examples of earnings management?

Examples of Earnings Management For example, assume a furniture retailer uses the last-in, first-out (LIFO) method to account for the cost of inventory items sold. FIFO creates a lower cost of goods sold expense and, therefore, higher profit so the company can post higher net income in the current period.

How do companies manipulate earnings?

There are two general approaches to manipulating financial statements. The first is to exaggerate current period earnings on the income statement by artificially inflating revenue and gains, or by deflating current period expenses.

How can earnings management be positive?

And contrary to the common wisdom that all earnings management is bad, researchers have identified a setting in which it can be good. “Firms with high-ability managers who smooth earnings have more-predictable earnings and cash flows, and the stock market incorporates that information into a firm’s stock price.

What are two tactics that a financial manager can use to manage earnings?

Earnings Management Techniques

- The big bath- This technique is often called a 1-time event.

- Cookie jar reserves – This technique is also an income smoothing technique.

- Operating activities – This earnings management technique occurs when managers plan certain events to occur in certain periods.

Is earnings management allowed under GAAP?

The accounting literature defines earnings management as “distorting the application of generally accepted accounting principles.” Many in the financial community (including the SEC) assume that GAAP deters earnings management. It is well known that financial report issuers prefer to report the highest income possible.

What are the primary methods of earnings management?

There are three types of techniques in earnings management they are; Aggressive & Abusive Accounting – This refers to the aggressive escalation of sales or revenue recognition. Abusive accounting includes cookie jar, big bath, etc., to show there is a high profit that year.

How do you manipulate profits?

Specific Ways to Manipulate Financial Statements

- Recording Revenue Prematurely or of Questionable Quality.

- Recording Fictitious Revenue.

- Increasing Income with One-Time Gains.

- Shifting Current Expenses to an Earlier or Later Period.

- Failing to Record or Improperly Reducing Liabilities.

How does earnings management relate to accounting quality?

In accounting, earnings management is a method of manipulating financial records to improve the appearance of the company’s financial position. Companies use earnings management to present the appearance of consistent profits and to smooth earnings’ fluctuations.

What is the difference between earning management and earning quality?

When management intervenes in the earnings reporting process in order to influence reported income numbers for their private gains, then managers have engaged in earnings management. That is, when managers do not intervene the earnings reporting process, earnings quality is high.

What are some ways to manage earnings?

Accounting Methods Used to Manage Earnings

- Cost flow assumptions. Choosing a cost flow assumption can affect profitability.

- Accrual accounting vs. cash basis accounting.

- Deferred tax estimates.

- Depreciation method.

- Capitalization practices.

- Acquisitions.

- Goodwill.

- The preparation of the statement of cash flows.

Is earnings management permissible under GAAP?

How do you calculate earnings quality?

The quality of earnings ratio compares reported earnings to cash flow from operations.

- Calculation. Quality of Earnings Ratio (%) = ((Earnings – Cash Flow from Operations) / Average Assets) x 100.

- Explanation.

- Example.

- Related Terms.

How can we detect earnings management?

Detecting Earnings Management

- Claiming revenue growth that doesn’t come with a corresponding growth in cash flows.

- Reporting increased earnings that only occur during the fiscal year’s final quarter.

- Expanding fixed assets beyond what is considered normal for the company and/or industry.

Why is earning management Bad?

Earnings management reduces the quality of financial reporting, it can interfere with the resource allocation in the economy and can bring adverse consequences to the financial market.

What is the difference between earning management and income management?

“Earnings management” is not a technical term in accounting or finance. However, it occurs when 1.) firm management has the opportunity to make accounting decisions that change reported income, and 2.) exploits those opportunities. Can you help by adding an answer?

How does earnings management affect a financial statement?

Earnings management takes advantage of how accounting rules are applied and creates financial statements that inflate or “smooth” earnings. Key Takeaways. In accounting, earnings management is a method of manipulating financial records to improve the appearance of the company’s financial position.

What’s the difference between positive accounting and earnings management?

Positive Accounting Theory suggests that accounting choice can be driven by efficiency reasons or managerial opportunism. When management intervenes in the earnings reporting process in order to influence reported income numbers for their private gains, then managers have engaged in earnings management.

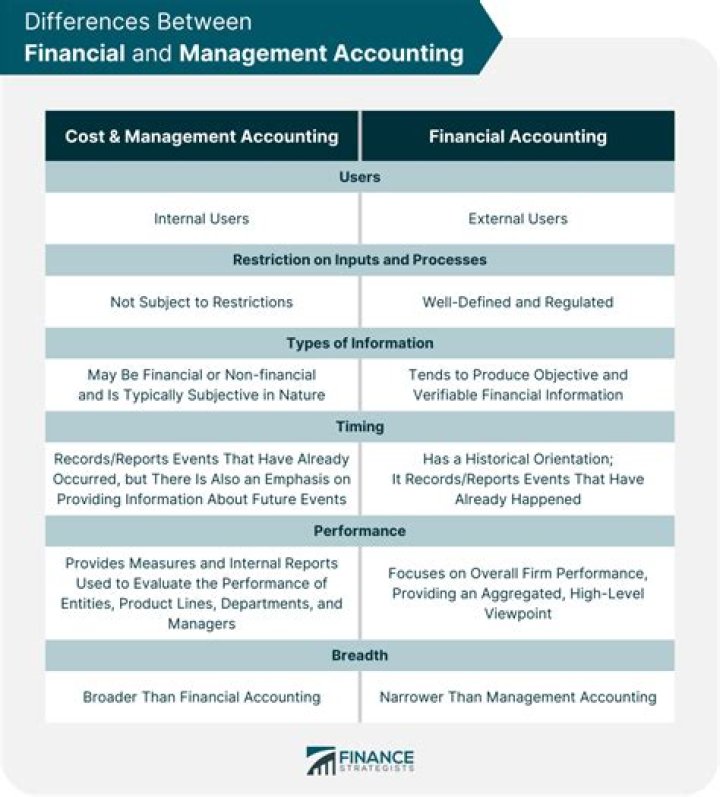

What’s the difference between management and financial accounting?

Financial and management accounting are two legs of accounting that provide the stakeholders of the business with a better financial picture of the organisation. It helps the managers in the decision-making process and helps them plan for the future.