What is the indirect effect of a change in accounting principle briefly describe the reporting of the indirect effects of a change in accounting principle?

The indirect effect of a change in accounting principle reflects any changes in current or future cash flows resulting from a change in accounting principle that is applied retrospectivelyIndirect effects are not included in the retrospective application, but instead are reported in the period in which the accounting …

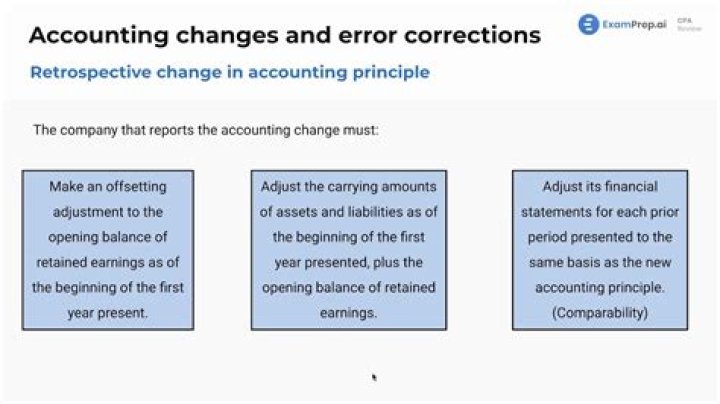

How do you disclose change in accounting principle?

If the change in accounting principle does not have a material effect in the period of change, but is expected to in future periods, any financial statements that include the period of change should disclose the nature of and reasons for the change in accounting principle.

What is the cumulative effect of a change in accounting principle?

The cumulative effect of an accounting change is a one-time adjustment and will not be offset in future years. In addition, the cumulative effect is the result of income measurements and should ultimately be included in retained earnings.

Why is it important to disclose changes in accounting principles and changes in reporting?

Understanding an Accounting Change The reporting entity could also change due to a merger or a breakup of a company. Accounting changes require full disclosure in the footnotes of the financial statements to describe the justification and financial effects of the change.

What are the major reasons companies change accounting principles?

The major reasons why companies change accounting methods are: (1) Desire to show better profit picture. (2) Desire to increase cash flows through reduction in income taxes. (3) Requirement by Financial Accounting Standards Board to change accounting methods. (4) Desire to follow industry practices.

Is a reclassification a change in accounting principle?

In such situations, the reclassification also is the correction of a misstatement. If the auditor determines that the reclassification is a change in accounting principle, he or she should address the matter as described in paragraphs 7 and 8 and AU sec.

What are the major reasons why companies change accounting principles?

What are the major reasons why companies change accounting methods?

What are the types of accounting errors?

What are the most common types of accounting errors & how do they occur?

- Data entry errors.

- Error of omission.

- Error of commission.

- Error of transposition.

- Compensating error.

- Error of duplication.

- Error of principle.

- Error of entry reversal.

What are the errors of principle?

Errors of principle are often simply accounting entries recorded in the incorrect account. The amounts are often correct, unlike an error of original entry. Oftentimes, the error of principle is a procedural error, meaning that the value recorded is correct but the entries are made in the wrong accounts.

What is the difference between errors and frauds?

The difference between fraud and error lies in the intention. Simply put, fraud is an act that is intentionally carried out to benefit certain individuals or groups and causes detrimental effect to others, while errors are acts of unintentional mistake or negligence.