What is the maximum debt-to-income ratio needed to qualify for a loan for a house?

Lenders prefer to see a debt-to-income ratio smaller than 36%, with no more than 28% of that debt going towards servicing your mortgage. 12 For example, assume your gross income is $4,000 per month. The maximum amount for monthly mortgage-related payments at 28% would be $1,120 ($4,000 x 0.28 = $1,120).

What percentage of debt-to-income ratio is good for mortgage?

Ideal debt-to-income ratio for a mortgage Lenders generally look for the ideal front-end ratio to be no more than 28 percent, and the back-end ratio, including all monthly debts, to be no higher than 36 percent.

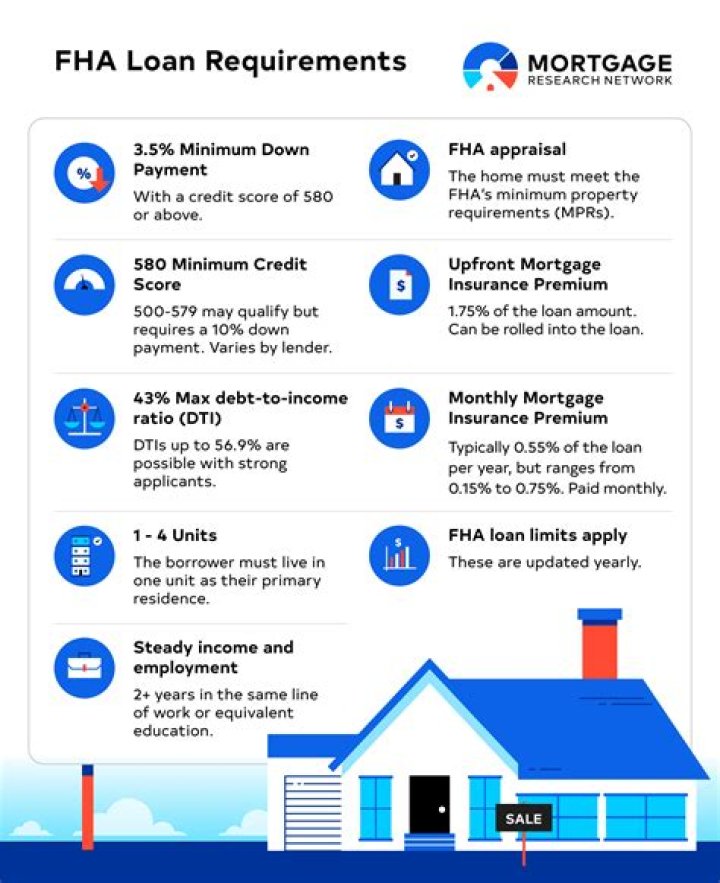

What’s the max debt-to-income ratio?

43%

As a general guideline, 43% is the highest DTI ratio a borrower can have and still get qualified for a mortgage. Ideally, lenders prefer a debt-to-income ratio lower than 36%, with no more than 28% of that debt going towards servicing a mortgage or rent payment. The maximum DTI ratio varies from lender to lender.

What is the average debt-to-income ratio?

What is an ideal debt-to-income ratio? Lenders typically say the ideal front-end ratio should be no more than 28 percent, and the back-end ratio, including all expenses, should be 36 percent or lower.

What should my debt to income ratio be?

If your gross monthly income is $6,000, then your debt-to-income ratio is 33 percent. ($2,000 is 33% of $6,000.) Evidence from studies of mortgage loans suggest that borrowers with a higher debt-to-income ratio are more likely to run into trouble making monthly payments.

Can you get a mortgage with a 43 percent debt to income ratio?

There are some exceptions. For instance, a small creditor must consider your debt-to-income ratio, but is allowed to offer a Qualified Mortgage with a debt-to-income ratio higher than 43 percent.

What’s the highest DTI ratio you can get for a loan?

By the way, 43% is the highest DTI ratio a borrower can get achieve and still be eligible to secure a loan. So, the lower the debt-to-income ratio, the more likely a borrower will not encounter any problems with paying off the debt.

What should my DTI be to pay down debt?

DTI of 0% to 35%: Your debt looks manageable. If your DTI is toward the higher end of this range, there are tips and tricks to pay down debt. DTI of 36 to 49%: Your debt management is adequate, but it could be causing you issues.