What is the meaning of assessable income?

‘Assessable income’ is your total income after deducting allowable expenses and approved donations. trade income for the accounting year; employment income; and. other income such as rental income, royalty income etc.

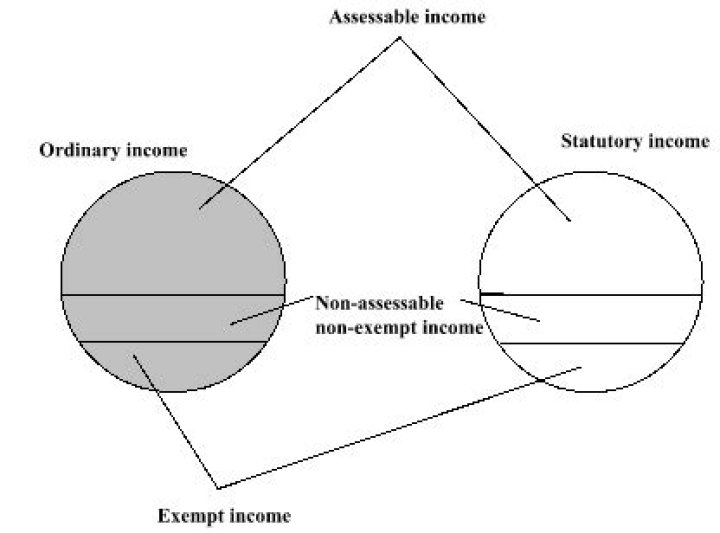

What is the difference between assessable income and taxable income?

Your assessable income is not the amount upon which your tax is calculated. The taxable amount, known as your ‘taxable income’ is the amount that is your assessable income less allowable tax deductions. Deductions, or legitimate expense claims, generally can be claimed if money was spent in order to earn income.

What is assessable income and some examples of assessable income?

dividends and other income from investments (for example, interest from term deposits and rent from an investment property) the annual total of more than $300 of non-cash benefits (property or services) received in payment for goods and services provided by the organisation.

Is assessable income the same as gross income?

Taxable income is your gross income minus allowable deductions. It’s the income you have to pay tax on. It includes income from: wages and salaries.

What is another word for assessable?

What is another word for assessable?

| computable | determinable |

|---|---|

| quantifiable | calculable |

| reckonable | quantitative |

| ascertainable | discoverable |

| countable | numerical |

What is not included in assessable income?

Non-assessable, non-exempt income is income that we do not assess and you don’t pay tax on. the tax-free component of an employment termination payment (ETP) genuine redundancy payments and early retirement scheme payments shown as ‘Lump sum D’ amounts on your income statement.

Is any of the income you provided assessable income?

The portion of all of the income you earn used to calculate your tax debt is called assessable income. But once you’ve eliminated credits and deductions, you get the amount of your income known as taxable income.

Is lump sum a assessable income?

Lump sum payments A lump sum payment is a one-time payment that is taxed and reported differently to your salary and wage income. You include lump sum payments as assessable income in your tax return in the financial year you receive the payment.

Which is the best definition of accessible income?

In general terms, your income is typically the money you earn from jobs that you work. But accessible income accounts for more than just your paycheck, as it includes most of the money you receive over a year. This definition of income is typically relevant on credit card applications.

How old do you have to be to report accessible income?

If you’re over 21, the options of what you can report as accessible income are wide enough to get the credit you need. Take the time to look at what you can report, and make sure you’re giving the credit card company the best possible view of your true financial situation. Jeff Gitlen is a graduate of the University of Delaware.

Can a loan be counted as accessible income?

In particular, loans or other forms of borrowed money. Whether you borrowed money from your mom or from Uncle Sam to pay tuition, don’t count it when calculating your accessible income. While there is no law against listing it, it doesn’t make sense to list it. After all, it’s debt and not income. How Do I Calculate My Accessible Income?

What does ” assessable income ” mean on a credit card?

Assessable income is basically all of the income that you pull in that could be taxed before you factor in things like tax deductions and credits. So it is usually higher than your taxable income. So just don’t get assessable income (which relates to taxes) mixed up with accessible income (which relates to credit card applications).