What is the method of computing depreciation?

Double-declining-balance method To apply the double-declining-balance (DDB) method of computing periodic depreciation charges you begin by calculating the straight-line depreciation rate. To do this, divide 100 per cent by the number of years of useful life of the asset. Then, multiply this rate by 2.

What is depreciation straight line method?

Straight line basis is a method of calculating depreciation and amortization, the process of expensing an asset over a longer period of time than when it was purchased. It is calculated by dividing the difference between an asset’s cost and its expected salvage value by the number of years it is expected to be used.

What is depreciation and methods of depreciation?

Depreciation is the accounting process of converting the original costs of fixed assets such as plant and machinery, equipment, etc into the expense. One such factor is the depreciation method. Thus, companies use different depreciation methods in order to calculate depreciation.

Are there other ways to calculate straight line depreciation?

Other Methods of Depreciation. In addition to straight line depreciation, there are also other methods of calculating depreciationDepreciation MethodsThe most common types of depreciation methods include straight-line, double declining balance, units of production, and sum of years digits.

What are the different types of depreciation methods?

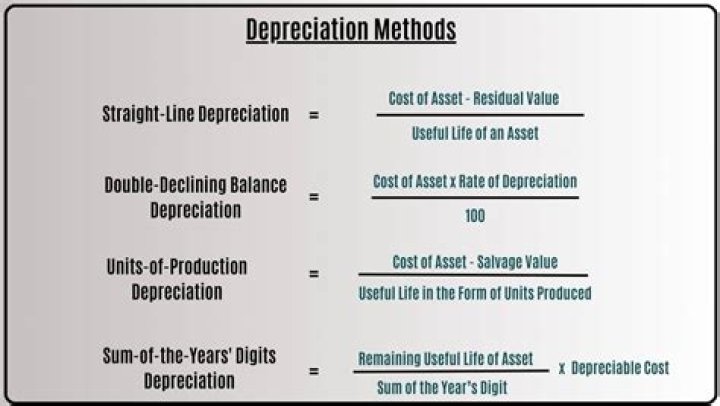

Depreciation Methods 1 Straight-Line Depreciation Method. 2 Double Declining Balance Depreciation Method. 3 Units of Production Depreciation Method. 4 Sum-of-the-Years-Digits Depreciation Method.

How is the DDB method used to calculate depreciation?

How is book value used to calculate depreciation?

Book value refers to the total value of an asset, taking into account how much it’s depreciated up to the current point in time. A note on useful life: if you’re calculating the amount of depreciation for tax purposes, the useful life figure should come from the IRS, which has sorted most depreciable assets into one of seven “property classes .”