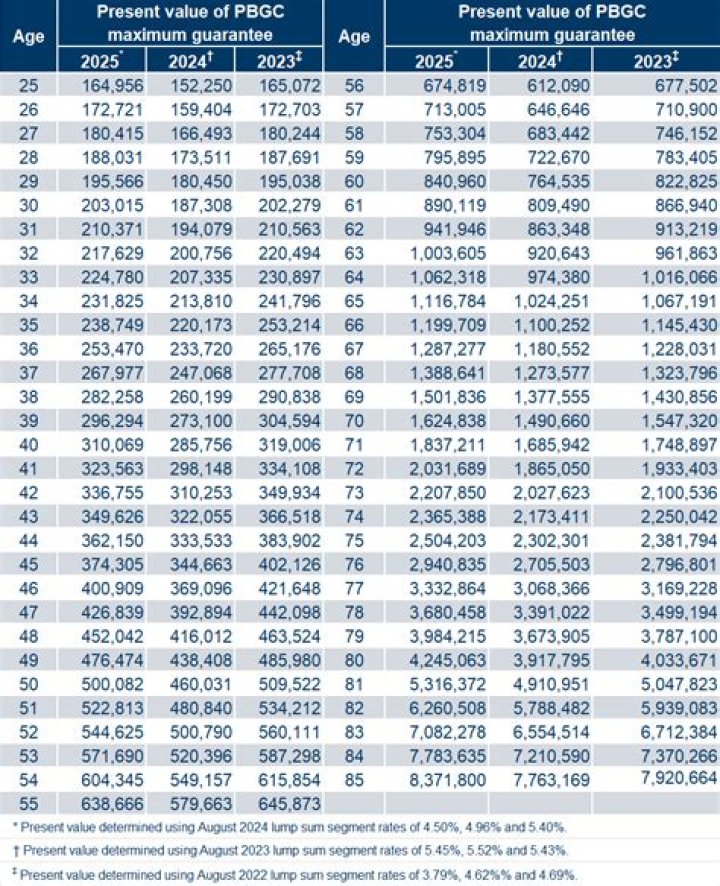

What is the PBGC rate?

Rates that change each calendar quarter

| Description | Most current rate(s) available |

|---|---|

| ERISA 4044 Annuities | Select rate – 1.82% for the first 20 years following the date of plan termination Ultimate rate – 1.68% thereafter. |

| Late Premium Payments | 3.00% |

| Late Withdrawal Liability | 3.25% |

What happens when PBGC takes over pension?

What happens when PBGC takes over as trustee of my plan? PBGC reviews your plan’s records to determine the benefits each person will receive. The amount we pay is subject to limits set by law. If you are already receiving a pension, we will continue paying you without interruption during our review.

Under what circumstances does the PBGC become involved in the administration of a retirement plan?

In FY 2020, PBGC paid monthly retirement benefits, up to legal limits, to more than 984,000 retirees in over 5,000 single-employer plans that ended. If a single-employer plan fails and PBGC becomes responsible for it, the agency directly pays benefits due to current and future retirees up to legal limits.

What is a PBGC premium?

PBGC is an independent agency not funded by general tax revenue. Instead, PBGC collects insurance premiums from employers that sponsor defined benefit pension plans, receives funds from the pension plans it takes over, and earns money from investments.

Can a defined pension be taken away?

Typically, employers that freeze their defined benefit plans will typically offer enhanced savings plans to their employees. Current law generally allows companies to change, freeze or eliminate altogether, their pension plans, so long as the benefits that employees have already earned are protected.

How many people are eligible for PBGC benefits?

PBGC paid benefits to 984,474 participants in 5,031 single-employer pension plans and 79,600 participants in 91 multiemployer plans. There is a statutory maximum benefit that PBGC can pay. Participants receive the lower of their benefit as calculated under the plan or the statutory maximum benefit.

What happens to your pension if your PBGC plan ends?

If your plan ends (this is called “plan termination”) without sufficient money to pay all benefits, PBGC’s insurance program will pay you the benefit provided by your pension plan up to the limits set by law. (Most people receive the full benefit they had earned before the plan terminated.)

How can I find out if my plan is covered by the PBGC?

The easiest way is to ask your employer or plan administrator for a copy of the “Summary Plan Description,” or SPD. The SPD will state whether your plan is covered by the PBGC program. Although we insure most defined benefit plans, some are not covered. federal, state, or local governments.

Is the PBGC a defined benefit or defined contribution plan?

The PBGC insures participants in private-sector defined-benefit plans, but not defined-contribution plans. The PBGC is funded not by government funds but by premiums charged to defined-benefit plan sponsors. The PBGC covers both single-employer plans and multiemployer plans.