What is the purpose of having adjusting entries?

The purpose of adjusting entries is to convert cash transactions into the accrual accounting method. Accrual accounting is based on the revenue recognition principle that seeks to recognize revenue in the period in which it was earned, rather than the period in which cash is received.

What is the purpose and importance of adjustments?

Adjusting entries allow the accountant to communicate a more accurate picture of the company’s finances. The owner can read through the financial statements knowing that everything that occurred during the month is reported even if the financial part of the transaction will occur later.

When should companies record the adjusting entries and why?

Adjusting entries are necessary because a single transaction may affect revenues or expenses in more than one accounting period and also because all transactions have not necessarily been documented during the period.

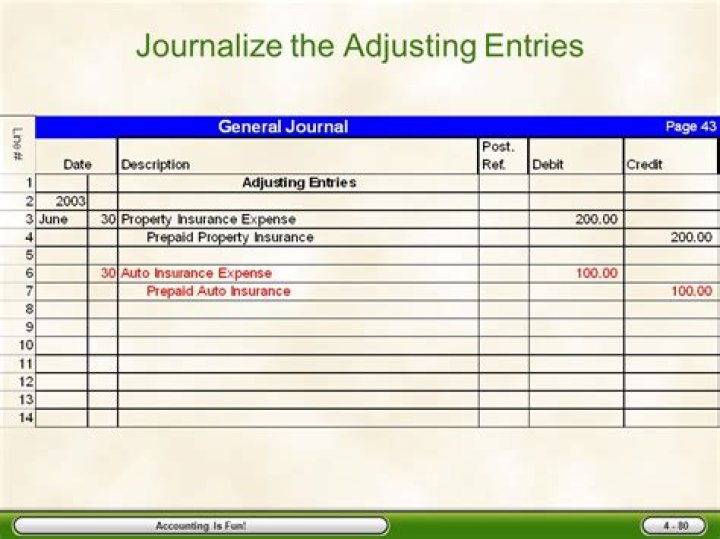

When adjusting entries are prepared?

Adjusting entries are made in your accounting journals at the end of an accounting period after a trial balance is prepared. After adjusted entries are made in your accounting journals, they are posted to the general ledger in the same way as any other accounting journal entry.

What Type of adjusting entry?

There are three main types of adjusting entries: accruals, deferrals, and non-cash expenses. Accruals include accrued revenues and expenses. Deferrals can be prepaid expenses or deferred revenue. Non-cash expenses adjust tangible or intangible fixed assets through depreciation, depletion, etc.

Which is the main purpose of adjusting entries?

The matching principle aims to align expenses with revenues. Expenses should be recognized in the period when the revenues generated by such expenses are recognized. The main purpose of adjusting entries is to update the accounts to conform with the accrual concept.

When do I need to update my adjusting entries?

Adjusting entries are journal entries made at the end of an accounting cycle to update certain revenue and expense accounts and to make sure you comply with the matching principle. The matching principle states that expenses have to be matched to the accounting period in which the revenue paying for them is earned.

What does it mean to adjust journal entry?

In summary, adjusting journal entries are most commonly accruals, deferrals, and estimates. Accruals are revenues and expenses that have not been received or paid, respectively, and have not yet been recorded through a standard accounting transaction.

When does an accounting entry need to be adjusted?

Adjusting entries are those accounting entries which are passed at the end of the accounting period. These entries are made to align the books of accounts to the matching concept and accrual principles laid down by accounting standards.