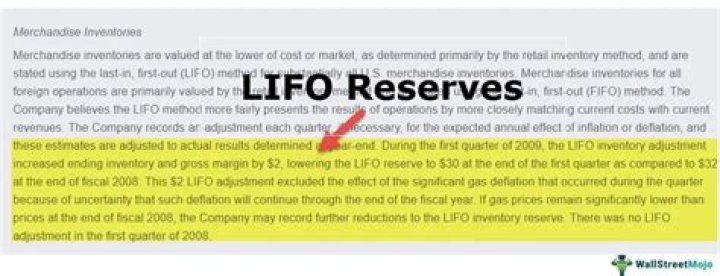

What is the purpose of LIFO reserve?

The LIFO reserve is an account used to bridge the gap between FIFO and LIFO costs when a company uses the FIFO method to track its inventory but reports under the LIFO method in the preparation of its financial statements.

What is LIFO layer liquidation?

LIFO layer liquidation occurs whenever a company which uses the LIFO inventory valuation method decides to reduce ending inventory to a level below beginning inventory. During inflationary periods, a company that allows this liquidation to occur will have to pay higher federal income taxes.

What is a LIFO layer and why does it matter?

LIFO is the acronym for Last-In, First-Out. When the end of the year quantity of inventory increases, the cost of the recently added units becomes a new layer—another LIFO layer. If the end of the year inventory quantity decreases, LIFO layers are “peeled away” starting with the latest (most recent) layer first.

How do you find the LIFO layer?

Calculate any increases in units of inventory for the next reporting period. Calculate the extended cost of these new units at base-year prices. Multiply the extended amount by the conversion price index to find the cost of the LIFO layer for the next reporting period.

What is the LIFO effect?

The change in the allowance from one period to the next is called the LIFO Effect. The LIFO effect is the adjustment that must be made to the accounting records in a given year.

Why does LIFO liquidation occur?

It occurs when a company that uses the last-in, first-out (LIFO) inventory costing method liquidates its older LIFO inventory. A LIFO liquidation occurs when current sales exceed purchases, resulting in the liquidation of any inventory not sold in a previous period.

How do LIFO layers work?

In essence, a LIFO system assumes that the last unit of goods purchased is the first one to be used or sold. This means that the most recent costs of acquired goods tend to be charged to expense quite soon, while the earlier costs of acquired goods linger in the costing records, possibly for years.

What is LIFO effect?

What is the LIFO allowance?

The LIFO reserve (also known as the allowance to reduce inventory to LIFO) is an account that represents the difference between the inventory cost computed for internal reporting purpose using a non-LIFO method and the inventory cost computed using LIFO method.

Can you switch between FIFO LIFO?

Most companies switching from LIFO to FIFO choose to restate their historical financial statements as if the new method had been used all along. It’s important that companies keep precise records to make these changes.

How can LIFO liquidation be prevented?

To overcome the problem of LIFO liquidation, some companies adopt an approach known as specific goods pooled LIFO approach. Under this approach, a number of similar products are combined and accounted for together. This combination or group of similar items is referred to as pool.

Is LIFO unethical?

LIFO understates profits for the purposes of minimizing taxable income, results in outdated and obsolete inventory numbers, and can create opportunities for management to manipulate earnings through a LIFO liquidation. Due to these concerns, LIFO is prohibited under IFRS.

Can you use LIFO and FIFO?

The Internal Revenue Service allows you to use the first-in, first-out method or the last-in, first-out method — FIFO and LIFO. If you choose LIFO, you can further select from one of several submethods, including dollar-value LIFO, or DVL.