What is variable cost in CVP analysis?

Cost-volume-profit (CVP) analysis is used to determine how changes in costs and volume affect a company’s operating income and net income. Variable costs per unit are constant. Total fixed costs are constant. Everything produced is sold. Costs are only affected because activity changes.

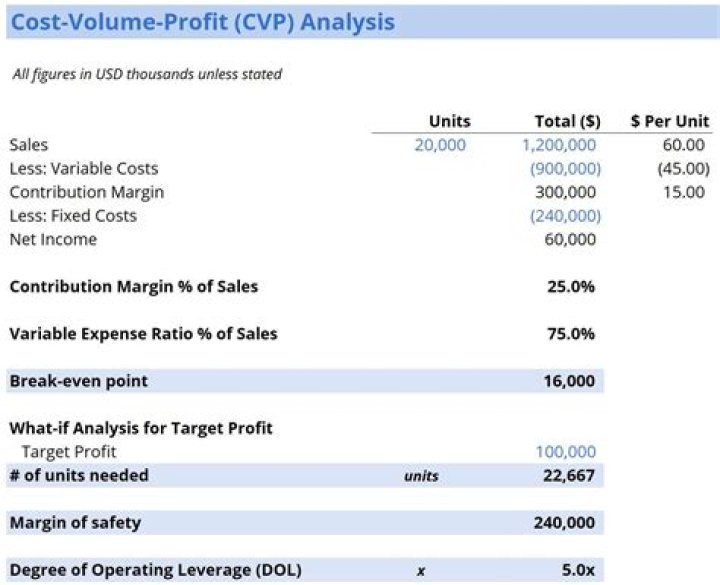

How is CVP analysis used in pricing?

Profit may be added to the fixed costs to perform CVP analysis on a desired outcome. For example, if the previous company desired an accounting profit of $50,000, the total sales revenue is found by dividing $150,000 (the sum of fixed costs and desired profit) by the contribution margin of 40%.

What is the CVP equation?

One of the main methods of calculating CVP is profit–volume ratio which is (contribution /sales)*100 = this gives us profit–volume ratio. contribution stands for sales minus variable costs.

What are the three variables Analysed by CVP?

In cost-volume-profit analysis — or CVP analysis, for short — we are looking at the effect of three variables on one variable: Profit. CVP analysis estimates how much changes in a company’s costs, both fixed and variable, sales volume, and price, affect a company’s profit.

How do you do CVP?

CVP is usually recorded at the mid-axillary line where the manometer arm or transducer is level with the phlebostatic axis. This is where the fourth intercostal space and mid-axillary line cross each other allowing the measurement to be as close to the right atrium as possible.

How CVP analysis is used in profit planning?

CVP analysis is a planning tool that management uses to predict the volume of activity, costs incurred, sales values, and profits received. In CVP analysis, we are looking at the effect of three variables (Costs, Sales volume & Sales Price) on one variable “Profit”.

What is the normal CVP?

A normal central venous pressure reading is between 8 to 12 mmHg. This value is altered by volume status and/or venous compliance.

How are fixed and variable costs classified in CVP?

Fixed and Variable Costs Cost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according . The contribution margin is the product’s selling price, less the variable costs associated with producing that product. The value can be given in total dollars or per unit.

Which is the best definition of Variable costing?

Variable costing refers to all direct cost and variable overhead incurred in the production/manufacturing of a product or rendering of service and excludes all fixed costs. Variable costing focus on all those costs which are directly impacted and affected by a change in production, unlike fixed cost which is static and stationary.

What is a cost-Volume-Profit Analysis ( CVP )?

Cost-Volume-Profit Analysis (CVP analysis), also commonly referred to as Break-Even Analysis, is a way for companies to determine how changes in costs (both variable and fixed) and sales volume affect a company’s profit.

How is variable costing used in mobile phones?

Since Variable Costing is focused only on Variable cost factors the per unit variable costing is computed as follows: For 50000 units all variable costs like Direct Material and Direct Labor will be 50% as the above cost is for 100000 units of mobile phones.