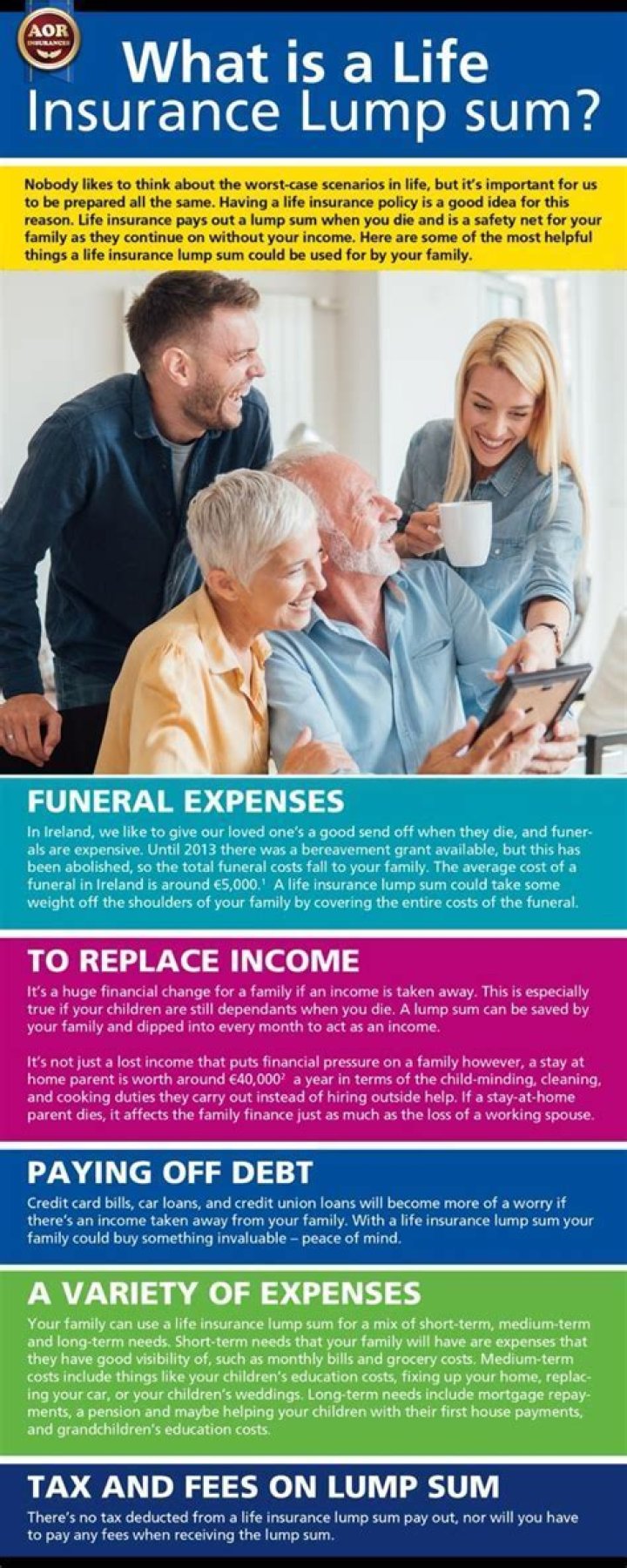

What part of the lump sum life insurance benefits are taxable?

Life insurance proceeds are not taxable with respect to income tax, so long as the proceeds are paid out entirely as a lump sum, one time, payment. However, if your beneficiary receives the life insurance payment as a series of installments, the insurer will typically pay interest on the outstanding death benefit.

How are life insurance distributions taxed?

Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren’t includable in gross income and you don’t have to report them. However, any interest you receive is taxable and you should report it as interest received.

Do you pay tax on lump sum life insurance?

If you have taken out life insurance to provide a lump sum or regular income to your loved ones when you die, there’s usually no income or capital gains tax to pay on the proceeds of the policy.

Is money received from a life insurance policy taxable?

Generally speaking, when the beneficiary of a life insurance policy receives the death benefit, this money is not counted as taxable income, and the beneficiary does not have to pay taxes on it.

Is money from a life insurance policy taxed?

Answer: Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren’t includable in gross income and you don’t have to report them. However, any interest you receive is taxable and you should report it as interest received.

Do you have to pay taxes on life insurance payouts?

If your estate is valued at $11.58 million – the IRS threshold for 2020 – or more, it will be subject to federal estate tax. This applies to life insurance payouts, too. To avoid this tax, consider transferring the policy to an irrevocable life insurance trust (ILIT).

What makes a withdrawal from a life insurance policy taxable?

In the life insurance industry this part is called the “policy basis.” Money that came from interest or investment gains. This portion is subject to income taxes. Your life insurance company will be able to tell you what amount in a withdrawal is “above basis” and taxable.

How is the taxable amount of life insurance calculated?

The taxable amount is based on the amount of the loan that exceeds your policy basis. Remember, policy basis is the portion you’ve paid in as premiums.

When to claim tax on lump sum distributions?

If you take a lump-sum distribution, even using Form 4972, the retirement plan administrator typically withholds 20% of your withdrawal and sends it to the IRS on your behalf. If your ultimate tax liability is lower than 20%, you can claim that part back when you file your taxes.