What represents the slope of the security market line?

market risk premium

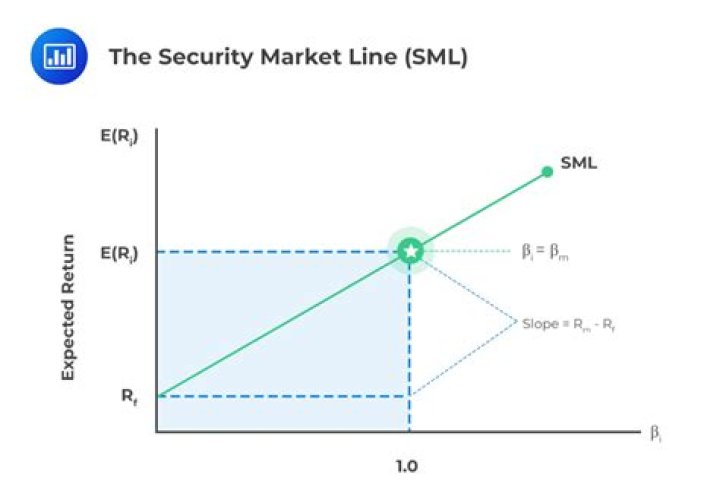

The slope of the security market line represents the market risk premium, i.e. the excess return over the market return. The market risk premium compensates for the additional systematic risk associated with the security.

How do you read a security market line?

The two-dimensional correlation between expected return and beta can be calculated through the CAPM formula and expressed graphically through a security market line, or SML. Any security plotted above the SML is interpreted as undervalued. A security below the line is overvalued.

What does the security market line depict quizlet?

What does the security market line depict? *Graphical depiction of the capital asset pricing model. It shows the relationship between expected return and beta.

How is capital market line calculated?

The Capital Market Line (CML) formula can be written as follows:

- ERp = Rf + SDp * (ERm – Rf) /SDm

- Suppose that the current risk-free rate is 5%, and the expected market return is 18%.

- Calculation of Expected Return of Portfolio A.

- Calculation of Expected Return of Portfolio B.

What is the measure of risk in security market line?

The beta of a security is a measure of its systematic risk, which cannot be eliminated by diversification. A beta value of one is considered as the overall market average.

What is the slope of the security market line SML )? Quizlet?

The slope of the SML, which is the difference between the expected return on a market portfolio and the risk-free rate. In other words, it is the reward investors expect to earn for holding a portfolio of beta of 1. Capital asset pricing model (CAPM)

What does the security market Line ( SML ) mean?

Updated Apr 4, 2019. The security market line (SML) is a line drawn on a chart that serves as a graphical representation of the capital asset pricing model (CAPM), which shows different levels of systematic, or market, risk of various marketable securities plotted against the expected return of the entire market at a given point in time.

What are the characteristics of the security market line?

Characteristics of the Security Market Line (SML) are as below SML is a good representation of investment opportunity cost, which provides a combination of the risk-free asset and the market portfolio. Zero-beta security or zero-beta portfolio has an expected return on the portfolio, which is equal to the risk-free rate.

What is the formula for plotting the security market line?

The formula for plotting the security market line is as follows: Required Return = Risk Free Rate of Return + Beta (Market Return – Risk Free Rate of Return)

Which is required return in security market line?

Required Return = Risk Free Rate of Return + Beta (Market Return – Risk Free Rate of Return) The security market line is commonly used by investors in evaluating a security for inclusion in an investment portfolio in terms of whether the security offers a favorable expected return against its level of risk.