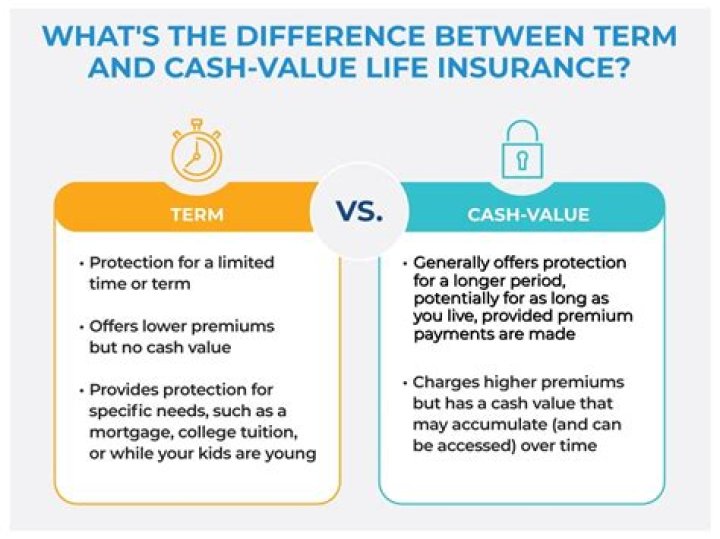

What should I do with the cash value of my life insurance policy?

Surrender the Policy for Cash Surrendering an insurance policy means you’re canceling the coverage. When you surrender a policy, you can get back the cash value minus any surrender charge. The insurance company will also subtract any unpaid premiums or outstanding loan balance.

What happens when you cash out an insurance policy?

You can usually withdraw part of the cash value in a whole life policy without canceling the coverage. Instead, your heirs will receive a reduced death benefit when you die. Typically you won’t owe income tax on withdrawals up to the amount of the premiums you’ve paid into the policy.

Can I withdraw fund value in insurance?

Don’t Throw Away Your Cash Value But if there is no need to pass the death benefit on to beneficiaries any longer, the policyholder can access the accumulated cash value while still alive, either by surrendering the policy entirely or by making smaller withdrawals or policy loans.

What to do with the cash value of a life insurance policy?

Generally, withdrawing your cash value will reduce your death benefit. Use it to pay your premiums Some life insurance policies allow you to use your cash value to pay your premiums.

Is it possible to cash out a life insurance policy?

Yes, cashing out life insurance is possible. The best ways to cash out a life insurance policy are to leverage cash value withdrawals, take out a loan against your policy, surrender your policy, or sell your policy in a life settlement or viatical settlement.

Can you skip premiums on cash value life insurance?

In an indexed universal life policy, you can pay a lower premium or skip premiums altogether if there’s enough cash value in the policy, says Sam Price, an independent agent & Broker with Assurance Financial Solutions.

What’s the cash value of universal life insurance?

For example, if you have a universal life insurance policy with a $200,000 death benefit and $100,000 in cash value, your goal is to completely empty the cash value and boost the death benefit to $300,000. That’s $100,000 more that will fall into your heirs’ hands instead of going to the life insurance company.