What will happen if the withholding agent fails to withhold final taxes?

As a withholding agent, you are personally liable for any tax required to be withheld. If you fail to withhold and the foreign payee fails to satisfy its U.S. tax liability, then both you and the foreign person are liable for tax, as well as interest and any applicable penalties.

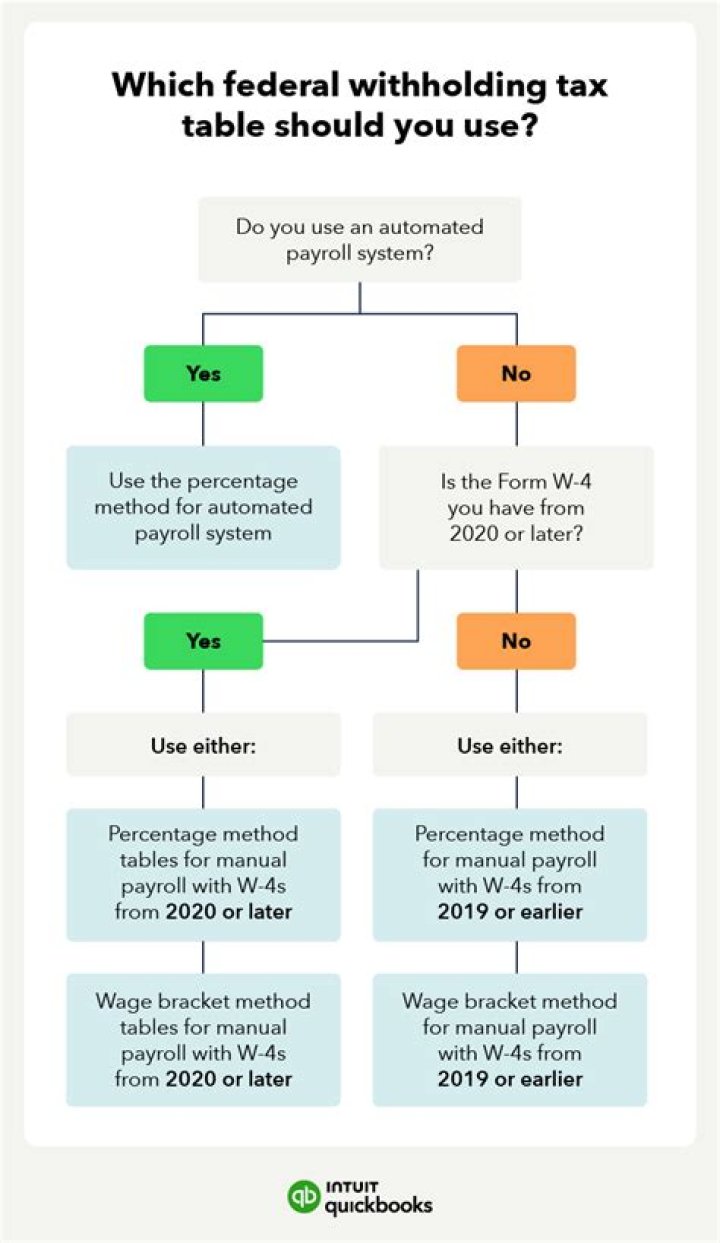

Is withholding tax fixed?

The amount of tax withheld on income payments other than employment income is usually a fixed percentage. In the case of employment income, the amount of withheld tax is often based on an estimate of the employee’s final tax liability, determined either by the employee or by the government.

How do I treat withholding tax in Quickbooks?

Here’s how:

- Go to the Accounting menu, and then choose Chart of Accounts.

- Click the New button.

- Select Other Expense from the Account Type drop-down menu.

- Choose Other Miscellaneous or Other Expense from the Detail Type drop-down list.

- Enter “Withholding Tax Expense” in the Name field.

- Click Save and close.

Can withholding tax be refunded?

In general, amounts withheld for US taxes are non-refundable. However, under certain circumstances, such as an incorrect rate being applied to withhold tax, a refund can be obtained.

Is withholding tax an expense?

Payroll Withholdings are Liabilities (The taxes withheld from employees are not an expense of the company that withheld them.) The payroll taxes that are not withheld from employees are expenses of the employer and are liabilities until the amounts are remitted.

How often do taxes have to be withheld on a 1042?

Taxes withheld must be deposited weekly, monthly, or annually (with the filing of Form 1042), depending on the amount of withheld taxes. A withholding agent who does not withhold when required can be liable for the tax that should have been withheld (IRC section 1461).

Who is required to withhold taxes from a business?

PERSONS REQUIRED TO WITHHOLD WITHHOLDING TAXES Individuals engaged in business or practiced of profession Non-individuals (corporations, associations, partnertship, cooperatives) whether engaged in business or not

When does a tax withholding agent have to withhold?

A withholding agent usually must withhold at the time of payment [Treasury Regulations section 1441.2 (e) (1)]. Taxes withheld must be deposited weekly, monthly, or annually (with the filing of Form 1042), depending on the amount of withheld taxes.

When does a law firm have to withhold payment?

In Private Letter Ruling (PLR) 200244017, the IRS determined that a law firm that had consulted with a foreign lawyer was a withholding agent and required to withhold on the payment to the foreign lawyer for his work in the United States.