When a company has bad debts expense it is considered?

Bad debt expenses are generally classified as a sales and general administrative expense and are found on the income statement. Recognizing bad debts leads to an offsetting reduction to accounts receivable on the balance sheet—though businesses retain the right to collect funds should the circumstances change.

What is an example of bad debt expense?

Example of Bad Debt Expense Company XYZ discovers that one of its customers, Big Store, is not doing very well. Big Store stops paying its bills and doesn’t pay Company XYZ for $100,000 worth of goods. Company is not confident that Big Store will ever pay, so it categorizes the $100,000 as a bad debt.

Why would a company overestimate bad debt expense?

As a result of not taking into account uncollectible customer accounts, overstating accounts receivable understates a company’s bad debt expense. When net income is closed to retained earnings at the end of an accounting period, retained earnings as an equity in the balance sheet is also overstated.

Is bad debt a direct or indirect expense?

Under the direct write-off method, bad debt expense serves as a direct loss from uncollectibles, which ultimately goes against revenues, lowering your net income. While it is arrived at through. For example, in one accounting period, a company can experience large increases in their receivables account.

How do you avoid bad debt expense?

How to prevent bad debt

- Put checks and balances in place.

- Make upfront payments your policy.

- Set your payment terms – and stick to them.

- Offer incentives for early payers.

- Up to date systems and processes.

- Stay in touch.

- Prevention is better than collection.

- Send out your invoices promptly.

Is Bad debts recovered an income or expense?

Bad debt recovery is a payment received for a debt that was written off and considered uncollectible. Bad debts must be reported to the IRS as a loss. Bad debt recovery must be claimed as part of its gross income.

How does a company account for bad debt expense?

The company usually uses the allowance method to account for bad debt expense as it excludes the accounts receivable that are unlikely to be recoverable in the report. This helps the company to have a more realistic view of its accounts receivable.

What are the two methods of recording bad debt expense?

The portion that a company believes is uncollectible is what is called “bad debt expense.” The two methods of recording bad debt are 1) direct write-off method and 2) allowance method. Bad Debt Direct Write-Off Method The method involves a direct write-off to the receivables

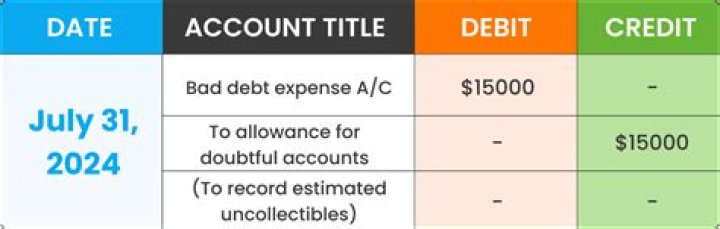

Which is an example of bad debt expense journal entry?

Allowance method. Under the allowance method, the company records the journal entry for bad debt expense by debiting bad debt expense and crediting allowance for doubtful accounts. For example, the company ABC Ltd. had the credit sales amount to USD 1,850,000 during the year.

When is a bad debt expense an uncollectible expense?

Bad debt expense is an expense that a business incurs once the repayment of credit previously extended to a customer is estimated to be uncollectible.